China's solid-state battery standard is all about V2G, not range

Issue 03: China's solid-state battery standard, BYD's 2027 production target, and the vehicle-to-grid endgame

China is standardising solid-state EV batteries with BYD starting production as soon as 2027. This is about unlocking the economics of full scale grid integration of EV batteries.

China is doing something that looks boring until you realise what it implies. It is moving solid-state batteries out of the lab and into the standards machinery.

Later this year Beijing is expected to publish a national standard for solid-state EV batteries, just as BYD and others begin real-world testing. BYD has floated production as early as 2027. Maybe that timetable slips. Most timetables do. But the direction is the point. If China standardises the technology while its manufacturers are scaling, solid-state does not arrive as a boutique upgrade for luxury cars. It arrives as a supply chain.

Most commentary will focus on the obvious benefits. More range. Faster charging. Better cold-weather performance. Those are real. They are not the interesting part.

The interesting part is what happens when millions of vehicles start behaving, economically, like grid assets.

V2G has been “almost here” for years. We have had clever bidirectional chargers for years. We have had software for years. What we have not had is a clean economic reason for ordinary owners to participate. The bottleneck is wear.

V2G’s bottleneck was wear

Vehicle-to-grid has always had an awkward truth at its centre. The grid wants you to cycle your battery, at least once and often twice, per day. Your battery would prefer that you didn’t.

Today’s common automotive chemistries degrade with use. That is normal. But grid participation adds extra cycling on top of driving. When you ask a rational EV owner to discharge for peak events or arbitrage, you are asking them to trade long-term value for short-term revenue.

If the expected cost of that extra wear is thousands of dollars in lost capacity and resale value, the compensation has to be more than a modest bill credit. That is why V2G has mostly stayed in pilots, enthusiasts, and tightly controlled programs.

In manifesto terms, degradation is an entropy tax. It turns useful work into lost future capability. You cannot eliminate it. You can only change its price.

Solid-state changes the price of cycling

Solid-state batteries promise the usual headline improvements: higher energy density, faster charging, longer life. The variable that matters most for V2G is cycle life.

Early lab results often cited for solid-state suggest something like 3,000 to 5,000 full cycles, perhaps double what many current automotive packs deliver in practice. Real-world performance may disappoint. The gap between lab cells and mass-produced packs is where optimism goes to die. But even a partial improvement changes the economics. If the depreciation cost per extra cycle falls, participation becomes easier to justify.

Once the cost per cycle falls, two things follow quickly.

Firstly, the revenue threshold for participation drops. Owners need less compensation to be indifferent, and aggregators can assemble more capacity without paying heroic incentives.

Secondly, V2G stops looking like a niche optimisation and starts looking like infrastructure. You can plan around it. Finance against it. Design programs that scale without constantly fighting the customer.

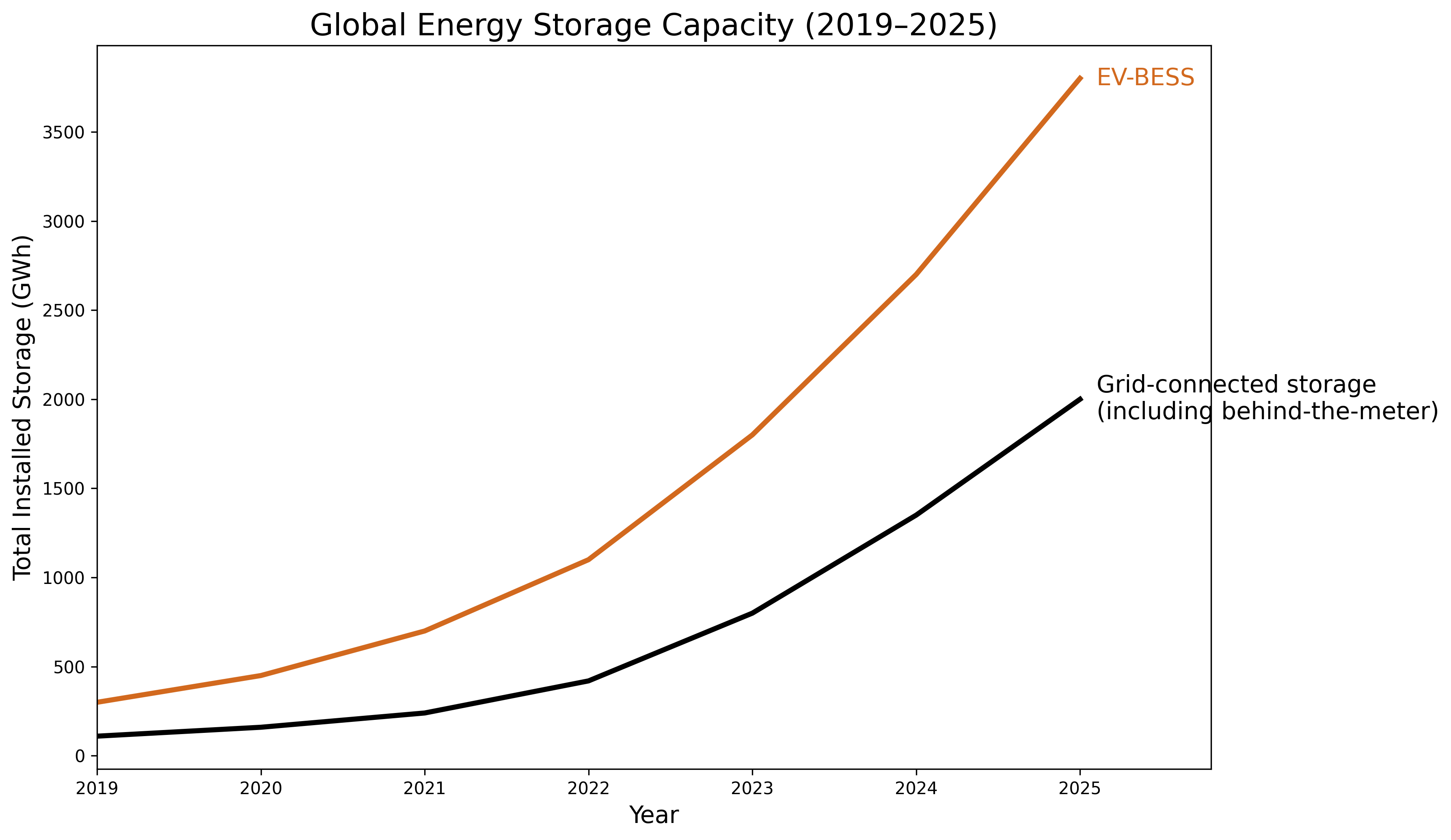

Sources: International Energy Agency (IEA), Global Energy Storage Outlook 2024; IEA, Global EV Outlook 2025; BloombergNEF, Energy Storage Market Outlook 2025; Benchmark Mineral Intelligence, 2025 global lithium-ion battery demand data. Stationary storage includes utility-scale and behind-the-meter systems. 2025 values include latest full-year installation estimates.

Sources: International Energy Agency (IEA), Global Energy Storage Outlook 2024; IEA, Global EV Outlook 2025; BloombergNEF, Energy Storage Market Outlook 2025; Benchmark Mineral Intelligence, 2025 global lithium-ion battery demand data. Stationary storage includes utility-scale and behind-the-meter systems. 2025 values include latest full-year installation estimates.

Over the past five years, global EV battery capacity has grown from roughly 300 GWh to nearly 2,700 GWh. Grid-deployed BESS is growing fast, but it is still an order of magnitude smaller. The centre of gravity in storage is not in substations. It is in vehicles. Even if only a fraction becomes dispatchable, the implications are structural.

China isn’t just building a better battery. It is trying to remove uncertainty.

The strategic move here is not just chemistry but the standard

A national standard sounds dull until you remember what fragmentation does to adoption. V2G is a coordination problem across layers that do not naturally cooperate: carmakers, charger manufacturers, networks, retailers, aggregators, and regulators. If each layer has its own protocol, safety envelope, and warranty carve-out, you do not get a market. You get a swamp.

A standard does not solve everything, but it drains a lot of uncertainty up front. It gives manufacturers a common target. It reduces interoperability risk. It simplifies compliance. It tells the supply chain what “compatible” means.

China has run this playbook before. It aligns the parts early, then scales.

If solid-state becomes a standardised platform inside the world’s largest EV manufacturing machine, competitors do not get the luxury of waiting for the perfect breakthrough. They have to respond to a shipped product.

The US is experimenting. China is industrialising.

Tesla’s “Powershare Grid Support” program in Texas is a good example of Western caution. It is a controlled entry: a big battery (Cybertruck), a volatile grid (ERCOT), and a structure that looks more like demand response than free-form wholesale participation.

That caution is rational. With today’s batteries, degradation costs are still real, warranties are sensitive, and the customer experience can be fragile. If you want to test V2G without creating a warranty nightmare, you start narrow.

China is moving in the opposite direction. It is pushing the enabling technology toward default status.

Australia is where this lands early

Australia sits in an odd position. We are not leading battery chemistry. We are exposed to the downstream consequences.

We have huge rooftop solar penetration, growing distribution constraints, and a transition that increasingly depends on flexibility. AEMO has been signalling for years that storage and dispatchable capacity are core infrastructure.

Now add market reality. Australia’s EV uptake is being driven heavily by Chinese manufacturers. If solid-state reaches scale in China first, Australia does not have to invent it. We import it.

That matters because the size of the V2G prize is extremely sensitive to cycling economics. When the per-cycle penalty drops, the bottleneck moves. The limiting factors become:

-

interoperability and safety standards

-

tariff design and customer incentives

-

aggregation rules and market participation models

-

distribution constraints and export limits

-

consumer trust, which complexity tends to destroy

The risk for Australia is not missing the hardware. It is importing the hardware and keeping nineteenth-century rules.

If V2G gets siloed by retailer and locked behind incompatible apps (I don't know about you, but I've got 11 charging apps on my phone), those “get paid while you park” carparks at commuter stations and shopping centres will stay theoretical for far too long.

As usual, technology will not be the brake. Imagination will.

What to build for

If you are building VPP or V2G infrastructure today, the takeaway is not “bet everything on solid-state.” The takeaway is to stop designing systems that assume batteries are too precious to touch.

Design for a world where cycling is cheaper, warranties are clearer, and participation is normal. In that world, value shifts from the pack itself to the coordination layer: software, dispatch confidence, customer experience, and market access.

Chemistry changes degradation. Degradation changes economics. Economics changes architecture. China is moving early on standards because it understands that chain.

Australia should take note. Not because we need to win a battery race, but because we need to stop letting 140 years of grid inertia decide what we call realistic.

The future will not arrive with speeches. It will arrive in containers, standards, and invoices. Then it will have felt obvious all along.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Australian Energy Market Operator. (2024, June 26). 2024 Integrated System Plan for the National Electricity Market. https://www.aemo.com.au/-/media/files/major-publications/isp/2024/2024-integrated-system-plan-isp.pdf

Australian Renewable Energy Agency. (2024, June 20). Batteries on wheels: Unlocking value for customers through smarter charging. https://arena.gov.au/news/batteries-on-wheels-unlocking-value-for-customers-through-smarter-charging/

Brogan, M. (2026, February 5). VFACTS: January off to a steady start. GoAuto. https://www.goauto.com.au/news/vfacts/sales-2026/vfacts-january-off-to-a-steady-start/2026-02-05/98421.html

Burrows, L. (2024, January 8). Solid state battery design charges in minutes, lasts for thousands of cycles. Harvard John A. Paulson School of Engineering and Applied Sciences. https://seas.harvard.edu/news/solid-state-battery-design-charges-minutes-lasts-thousands-cycles

enX. (2025, February 12). National Roadmap for Bidirectional EV Charging. Australian Renewable Energy Agency. https://arena.gov.au/assets/2025/02/Bidirectional-Bidi-ROADMAP-2025-01-15-1.pdf

Federal Chamber of Automotive Industries. (2026, February 5). Australian new vehicle sales for January 2026 [Media release]. https://www.fcai.com.au/news/index/view/news/australian-new-vehicle-sales-for-january-2026

Huang, W.-Z., Liu, Z.-Y., Xu, P., Kong, W.-J., Huang, X.-Y., Shi, P., Wu, P., Zhao, C.-Z., Yuan, H., Huang, J.-Q., & Zhang, Q. (2023). High-areal-capacity anode-free all-solid-state lithium batteries enabled by interconnected carbon-reinforced ionic-electronic composites. Journal of Materials Chemistry A, 11, 12713–12718. https://doi.org/10.1039/D3TA00121K

Kang, L. (2025, February 15). BYD expects to begin “demonstration use” of all-solid-state batteries by 2027, exec says. CnEVPost. https://cnevpost.com/2025/02/15/byd-demonstration-use-all-solid-state-batteries-2027/

Kang, L. (2025, December 31). China begins seeking public input on national standard for EV solid-state battery. CnEVPost. https://cnevpost.com/2025/12/31/china-seeking-public-input-national-standard-ev-solid-state-battery/

State Administration for Market Regulation. (2025). Solid-state battery for electric vehicle—Part 1: Terms and classification (National standard project; plan no. 20250835-T-339) [Database entry]. National Public Service Platform for Standards Information. https://std.samr.gov.cn/gb/search/gbDetailed?id=a74282e3ed2b16eaa5b51fb314d72f7f

Tesla. (n.d.). What is Powershare Grid Support? Retrieved February 21, 2026, from https://www.tesla.com/support/powershare/what-is-powershare-grid-support

Xu, C., Behrens, P., Gasper, P., Smith, K., Hu, M., Tukker, A., & Steubing, B. (2023). Electric vehicle batteries alone could satisfy short-term grid storage demand by as early as 2030. Nature Communications, 14, 119. https://doi.org/10.1038/s41467-022-35393-0

Ye, L., Lu, Y., Wang, Y., Li, J., & Li, X. (2024). Fast cycling of lithium metal in solid-state batteries by constriction-susceptible anode materials. Nature Materials, 23, 244–251. https://doi.org/10.1038/s41563-023-01722-x

Zhang, C., Wang, X., Wang, Y., & Tang, P. (2025). Economic viability of vehicle-to-grid (V2G) reassessed: A degradation cost integrated life-cycle analysis. Sustainability, 17(12), 5626. https://doi.org/10.3390/su17125626

Discussion

Loading comments...