Massachusetts uses energy markets to reduce copper build-out

Issue 04: National Grid's DER marketplace in Massachusetts tests whether markets can solve grid constraints

National Grid's new DER marketplace in Massachusetts is testing a fundamental question: can distributed energy resources solve grid bottlenecks more cheaply than traditional infrastructure—and can markets coordinate them efficiently enough to matter?

Massachusetts runs an expensive grid. Residential electricity prices have been pushing past 30 cents per kilowatt-hour, roughly twice the US average, and network costs are a major driver.

When a local part of the system gets tight, the response is familiar. Upgrade the feeder. Reinforce the substation. Add the capital to the rate base. Recover it over thirty years. The logic is simple. Concrete lasts. Copper lasts. Regulators understand assets you can point to.

National Grid, the major local utility, is testing a different response. Instead of building first, it is asking whether it can buy flexibility instead.

Late last year it launched a non-wires alternatives procurement marketplace built on Piclo, a digital energy marketplace for flexible energy resources. Aggregators can bid batteries, demand response, managed EV charging and other distributed energy resources against specific local constraints. Not vaguely. Not “somewhere in the region.” In the place where the network is tight, in the season it binds, in the hours that matter. If a portfolio of DERs can defer a $15 million substation upgrade for several summers, that deferral has real value. It may be cheaper than steel and copper. It is certainly faster.

Economists call this locational non-wires alternatives. In plain language, it turns congestion from an engineering fate into a service you can contract for.

A nodal market, and still not enough

Australians should note something important. Massachusetts sits inside ISO New England, which runs a nodal wholesale market. Energy clears using locational marginal pricing. Prices reflect congestion and losses at specific transmission nodes. That is already more granular than Australia’s five-region NEM. And still it is not granular enough.

Even in a nodal market, the nodes are on the bulk grid. They reach transmission substations and transmission-connected buses. They do not economically clear the distribution network. They do not reach the pole-top transformer at the end of your street. The last miles remain administratively planned rather than economically coordinated.

Wholesale LMP can tell you a zone is tight. It cannot guarantee two megawatts of managed EV charging on a specific feeder between four and eight on a humid August evening. It cannot procure that outcome. It was never designed to.

The Piclo marketplace is an attempt to add a coordination layer beneath the wholesale market. Not to replace nodal pricing. To complement it. Above the substation, price clears continuously. Below it, coordination defaults to engineering planning and blunt tariff signals. Piclo does not push LMP downward. It inserts a different instrument, targeted procurement, into a layer that wholesale markets do not clear.

If it works, it is an architectural shift. The grid becomes layered. High-voltage coordination through wholesale prices. Low-voltage coordination through local flexibility contracts. One physical system. Two coordination mechanisms. Different scales. Different tools.

Market design meets the distribution network

This is not a generic DER tender. The power of the model is specificity.

The utility defines the constraint. Location. Season. Hours. Performance requirements. Then bids compete to solve the same problem. That changes the upgrade decision tree.

Instead of treating infrastructure as the default and flexibility as a pilot program, both options sit side by side. If aggregated DERs can reliably deliver peak reduction at lower cost, the capital project moves down the queue.

The time difference alone is material. A traditional network upgrade can take three to five years from planning to commissioning. A distributed portfolio can be assembled in twelve to eighteen months. In an economy that is electrifying quickly, that speed matters.

The aggregator’s bottleneck is not technology. It is bankability.

Batteries, demand response and managed EV charging already work. The hard part is finance. DER portfolios usually need more than one revenue stream. A utility contract for local services. Wholesale participation where permitted. Retail program value. For the asset to be built, at least one of those streams must be stable and multi-year. Short-term procurement does not finance ten- to fifteen-year assets.

That is why multi-year contracts with performance guarantees matter. The utility is underwriting flexibility deployment in exchange for deferring its own capital expenditure. If structured properly, both sides win. Lower system cost. Lower timing risk. Less bill shock.

The economics is compelling

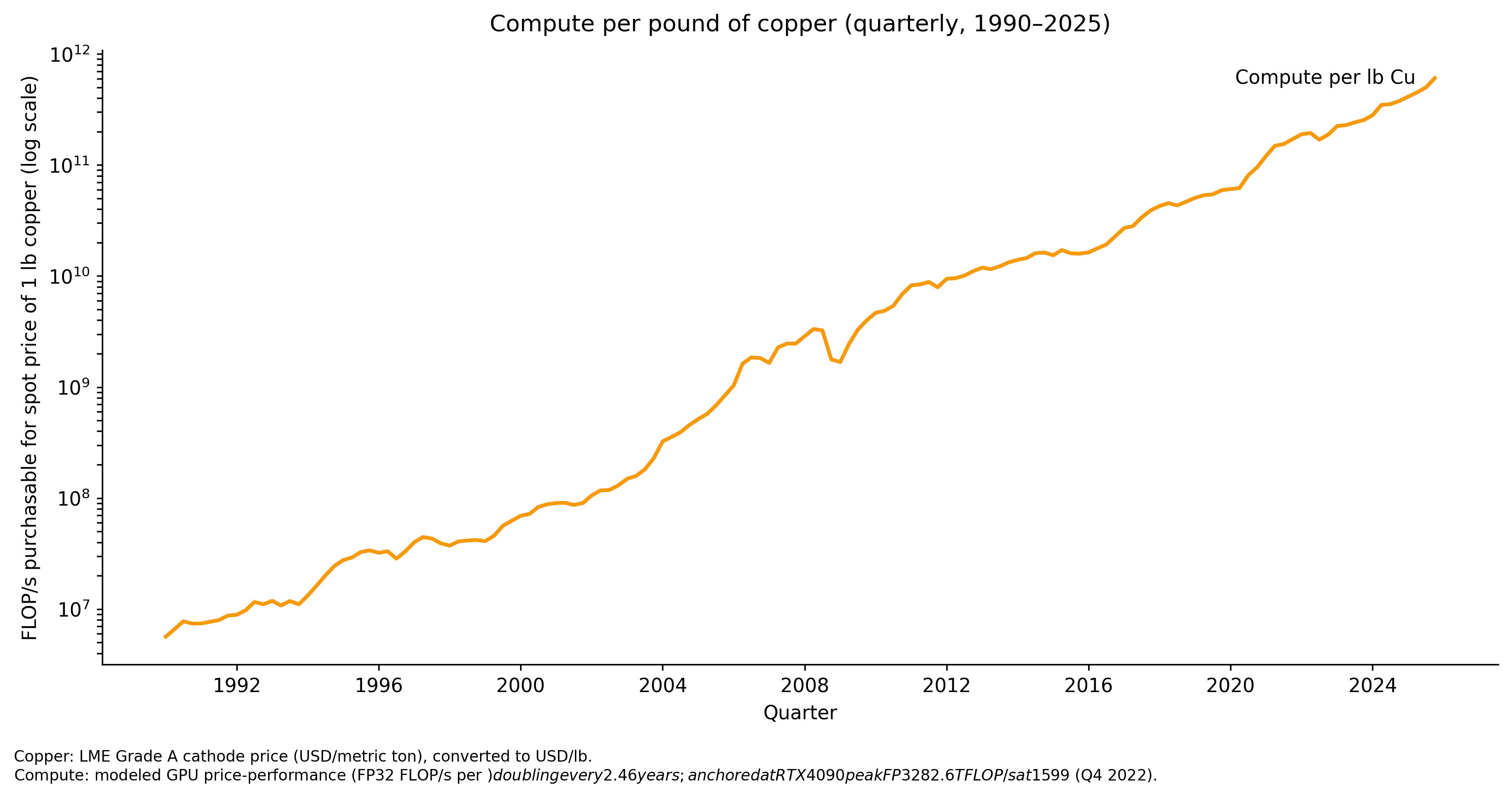

Simplistically, we are replacing copper with compute here.

That looks like a fairly straight line but, hey that's a logarithmic scale on the left of the chart. One pound of copper at the end of 2025 actually buys 108,000 times as much compute as it did in 1990. The Electric Slide has a 99% price decline over the same period - compute-in-copper-terms is 99.999% cheaper!

This will test regulation

The biggest obstacle is not engineering. It is incentives.

Utilities earn returns on capital deployed. A $15 million substation enters the rate base and produces regulated returns for decades. A contracted flexibility service does not fit the model as neatly.

Unless regulators allow clean cost recovery for contracted DER services, and treat avoided capital as success rather than lost opportunity, the bias toward building will persist.

Markets alone cannot overcome a framework that rewards concrete and copper more than orchestration. Massachusetts is testing whether that framework can evolve.

Why this matters for Australia

This experiment is not about one state. It is about whether grids can adapt structurally without bankrupting customers.

Massachusetts already has nodal wholesale pricing. It already prices transmission congestion. And it still needs a distribution-level coordination mechanism. That should resonate elsewhere.

In Australia, the NEM wrestles with how to value flexibility in a market architecture designed for centralised generation. Distribution constraints are mostly handled through administrative planning rather than competitive procurement.

Massachusetts is pointing toward the next layer of market evolution. Wholesale pricing at the top. Distribution flexibility markets beneath. Both coordinating the same physical system at different scales.

The question is simple but profound. Can we coordinate thousands of distributed assets faster and cheaper than we can build new copper?

If the answer is yes, grid modernisation becomes a coordination challenge rather than a construction race.

If the answer is no, electrification will keep arriving as bill shock, because we will keep trying to solve software-speed problems with civil-works timelines.

Massachusetts is testing whether markets can reach deeper into the grid than they ever have before. The outcome will tell us how adaptable modern electricity systems really are.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

AEMC. (2018). Coordination of generation and transmission investment (CoGaTI) – Final report. Australian Energy Market Commission.

AEMC CoGATI Final report Dec18

Electric Slide. (2024). The economics of distributed flexibility markets. Electric Slide. https://www.electricslide.com

ISO New England. (2024). Wholesale electricity markets and pricing. https://www.iso-ne.com/markets-operations

Massachusetts Department of Public Utilities. (2024). Electric distribution rate filings and tariffs. https://www.mass.gov/orgs/department-of-public-utilities

National Grid. (2023). Local flexibility markets and Piclo procurement platform overview. https://www.nationalgridus.com

Piclo. (2024). Piclo Flex: Enabling distributed energy flexibility markets. https://www.piclo.energy

U.S. Energy Information Administration. (2024). Electric power monthly – Retail electricity prices. https://www.eia.gov/electricity/monthly

London Metal Exchange. (2024). Historical copper prices. https://www.lme.com

Our World in Data. (2024). Semiconductor performance and computing cost trends. https://ourworldindata.org

Ferguson, A. (2026). Compute per pound of copper dataset (1990–2026). Battling Entropy Research Archive.

Discussion

Loading comments...