Connection Pending

Issue 08: Why Australia's EV charging rollout is stalled by 18–36 month grid connection delays

Grid connection delays of 18–36 months and costs of hundreds of thousands of dollars per site are throttling fast charger deployment in Australia, particularly in the bush. EV sales are rising quickly. Infrastructure is not. The constraint is not capital. It is connection. We need a dedicated funding programme for long-distance charging infrastructure.

I used to think range anxiety was mostly solved. Last week I was driving to Canberra. Somewhere between Lake George and the outskirts of the city the car went "ping". 5% battery. I had missed it completely. We found a charger and crept in at 1%.

The good old days are gone

For a brief period, the system worked. Between 2019 and 2022, Tesla effectively bundled cars and infrastructure. It had close to 50% market share and built out its Supercharger network in parallel. If you bought the car, the system worked. That structure has disappeared.

By 2024, Chinese brands led by BYD had taken more than 20% share and, together with MG, Polestar and GWM, now dominate new EV sales. Tesla is closer to 20%. None of these other manufacturers are building national charging networks. Infrastructure has been pushed to third parties. The economics are weaker. The incentives are fragmented.

The numbers look fine, until they don't

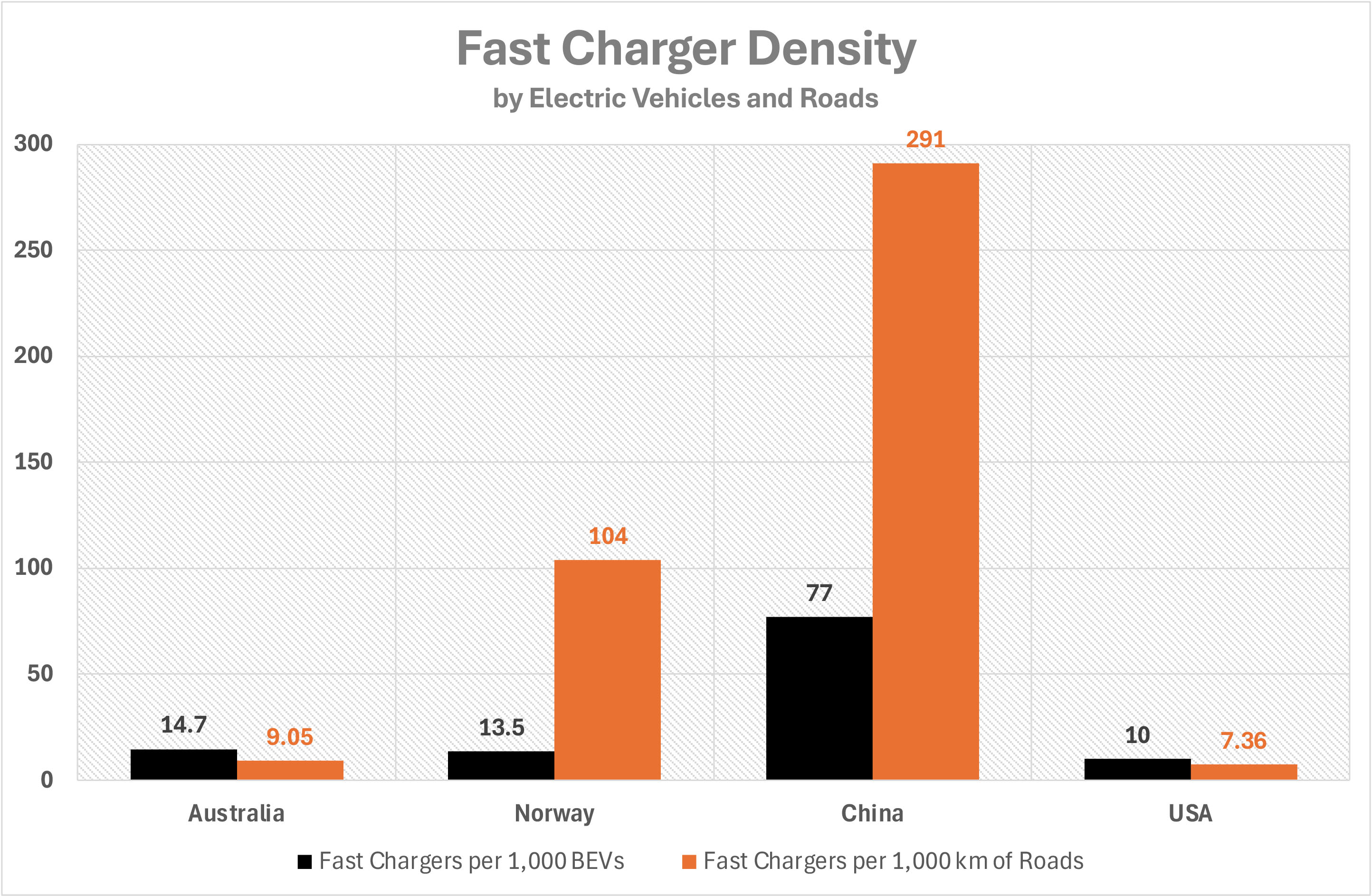

On a per vehicle basis, Australia's charging looks comparable to leading markets. Around 300,000 battery electric vehicles (BEVs) and 4,192 fast charging plugs gives 14.7 chargers per 1,000 vehicles. Norway, admired as "EV heaven", sits at 13.5. On that metric, we are not behind.

But that is the wrong denominator. Australia has long distances and a dispersed road network. What matters is coverage. On that measure, Australia has 9 fast chargers per 1,000 km of roads. Norway has over 100. China has 291. We do not have too few chargers per car. We have too few chargers per kilometer.

The constraint is connection

The bottleneck is not manufacturing capacity. It is not capital. It is grid connection.

A modern 350kW fast charging site behaves like a small industrial load. In metropolitan areas, the obvious locations are already constrained. Connecting new capacity requires network upgrades, new transformers, feeder work, or substation augmentation. The process is slow. Application queues run 18 to 36 months in many jurisdictions. Costs are often in the hundreds of thousands of dollars per site.

For operators, this breaks the model. Capital is committed up front. Revenue depends on uncertain utilisation. Timing is outside their control. Ampol is the cleanest example. It has capital, sites and demand. It is still rolling out more slowly than planned. The issue is not willingness to build. It is the difficulty of connecting.

One metro problem, one highway problem

It helps to separate two different systems.

In cities, fast charging is a hosting capacity and process problem. Demand exists. The challenge is that the best sites are constrained, approvals are fragmented, and connections are slow and bespoke. This is fixable with better information, standard connection products, battery deployment to buffer demand and more flexible use of existing network capacity.

Highways are different. Demand is thin, distances are long, and utilisation is uncertain. Here, the problem is not just connection timing. It is who pays for the backbone.

The coordination problem

No single player now has both the incentive and the balance sheet to build ahead of demand. Third-party operators must guess where demand will be in three years, commit capital today, and then wait two years for connection. Get it wrong and you strand assets. Get it right and you still wait.

International models

Three countries show how governments can break this impasse — and what happens when they don't.

Norway co-invested early and systematically. A dedicated public fund backed charging infrastructure along key corridors from the early 2010s, creating the confidence private operators needed to follow. Government money was not trying to build everything; it was trying to make the first movers viable. It worked. Norway now has over 100 fast chargers per 1,000 km of roads, charging infrastructure is treated as part of the transport system, and EV adoption is the highest in the world by share of new sales.

China took a different approach: it threw money at the problem and built well ahead of demand. The result is 291 fast chargers per 1,000 km of roads and few coverage gaps on the national highway network. Utilisation was poor for years. The infrastructure is there regardless.

The United States shows what happens without coordination. Federal investment through the NEVI programme has been substantial, but it has flowed toward urban and suburban markets where commercial returns are clearest. The interior remains patchy. Dense coastal clusters. Empty roads in between.

Australia is drifting toward that state. EVs will be viable in Sydney and Melbourne and utterly impractical in the bush. That is not a good outcome for our fuel security, the environment or the anti-entropy rebellion.

The scale is manageable

Australia currently has about 9 fast chargers per 1,000 km of roads.

Getting "halfway to Norway" would mean roughly 50. On today's geometry, that implies moving from about 4,200 fast charging plugs to roughly 23,000 — around 19,000 additional plugs, or about 5,800 additional sites at current densities.

What does the electrical backbone cost? I estimate current connection costs at around A$500,000 per site. That is broadly consistent with the connection cost data in DCCEEW's 2025 report on streamlining EV infrastructure connections. Sites in the bush, which is where most of the 5,800 new locations need to go, are more expensive. Call it A$700,000 per site once longer feeder runs, transformer upgrades and civil works are counted.

5,800 sites at A$700,000 is A$4.06 billion. Call it A$4 billion. Spread over 5 years, that is A$800 million per year. Network planners with a better estimate please chime in on the comments.

A$4 billion is not a large number in Australian infrastructure terms. The 5-year total is roughly comparable to a single year of distribution network capital expenditure. The issue is not affordability. It is structure.

Australia has grant programmes for EV charging infrastructure, most notably $199 million in NSW. But that barely touches the sides of the problem. We do not yet have a funding architecture commensurate with the scale of the corridor-electrification task.

Who pays?

Australia often frames EV policy around a simple question: petrol drivers fund the roads through fuel excise, so EV drivers should pay their share.

It is a reasonable instinct but a complicated reality. Fuel excise raises around A$25–30 billion per year, but it is not a clean road charge. It flows largely into general revenue and is partially offset by fuel tax credits. Road funding is already a mix of user charges and general taxation.

The equity objection, that taxpayers should not subsidise infrastructure used mainly by wealthier early adopters, deserves a direct answer rather than a sidestep. The honest response is that Australia routinely socialises the upstream infrastructure that makes competitive markets possible: electricity transmission, roads, ports, airports. Fast charging corridors are not a retail service. They are transport infrastructure. They play the same enabling role as lanes, interchanges and service centres. The question is not whether EV drivers should eventually pay their share. They should, through road user charges as the fleet transitions. The question is who funds the backbone that makes the network commercially viable in the first place. That is a legitimate infrastructure question, not an EV subsidy question.

The right model

Australia does not need to "go full China" and socialise every charger. It needs to underwrite enough of the upstream corridor capacity to make competitive fast-charging rollout financeable.

Designate the corridors. Build shared electrical capacity at priority nodes. Treat that capacity as infrastructure. Let everything else compete.

Entropy wins by waiting

There is no shortage of capital. There is no shortage of vehicles. There is no shortage of demand. Energy is available. Capital is available. The system still does not build.

The grid connection bottleneck is solvable, but it requires governments and distribution businesses to treat EV charging as infrastructure that enables a market, not as just another customer request. Until that shift happens, Australia's 9 chargers per 1,000 km of roads will remain an anchor on adoption, the gap between us and our peer markets will widen, and we will remain hostage to every drone in the Strait of Hormuz.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Ampol Limited. (2024). Annual report 2024. Ampol Limited. (2025). Annual report 2025.

Australian Energy Regulator. (2024). Electricity and gas networks performance report 2024.

Australian Renewable Energy Agency. (2024). Insights from ARENA’s public charging projects.

Brogan, M. (2026, February 5). VFACTS: January off to a steady start. GoAuto.

Clean Energy Finance Corporation. (2024). Ampol accelerates future fuels push with clean energy focus.

Department of Climate Change, Energy, the Environment and Water. (2025a). National electric vehicle strategy: Annual update 2024–25.

Department of Climate Change, Energy, the Environment and Water. (2025b). Streamlining the connection of EV charging infrastructure and large CER: Recommendations report.

Electric Vehicle Council. (2025a, July 4). EV sales power ahead in 2025.

Electric Vehicle Council. (2025b, October 14). Australia makes gains in EV uptake but faces steep road ahead, report finds.

Electric Vehicle Council. (2026, January 8). EV sales hit record highs in 2025 with 38% rise and new monthly record in December.

Energy Consumers Australia, & HoustonKemp. (2025). Creating accessible and affordable public EV charging networks in Australia.

Fallah, A. (2026, January 5). Tesla Australia sales slump in 2025, dragged down by Model 3. CarExpert.

Infrastructure Australia. (2023). National highway electric vehicle fast charging network.

Stopford, W. (2026, January 7). Australia’s best-selling EVs in 2025 revealed. CarExpert.

Discussion

Loading comments...