Why Australia needs locational pricing

Issue 15: Australia's electricity market needs better price signals that reflect local conditions

Australia’s electricity prices ignore location, even though the grid doesn’t. This mismatch drives congestion, curtailment, and inefficient investment. There is a better system used in much of the world. Locational marginal pricing aligns prices with physics, improving coordination of batteries, generation, and demand. It adds complexity, but the cost of today’s overly simple price signals is rising as the system becomes more distributed and constrained.

Australia’s electricity market was not designed for the system we are now building. It was designed for a world of large generators, predictable flows, and relatively stable demand, where a handful of regional prices could reasonably approximate what was happening across the grid. That world is fading quickly. In its place is something far more dynamic: millions of rooftop systems, rapidly growing batteries, increasingly binding transmission constraints, and flows that shift not just seasonally, but hourly. The physical system has fundamentally changed, but the way we price it has not.

At the heart of the issue is a simple mismatch. Electricity is inherently local. It is produced at a specific point, consumed at another, and transported across a network that has limits. Those limits matter. When a line is congested, electricity cannot flow freely, and the value of energy on one side of that constraint diverges from the value on the other. Yet in the National Electricity Market, we compress all of that complexity into a single price per region. Five regions, broadly aligned with the NEM states, five prices, and within each, a vast amount of hidden variability.

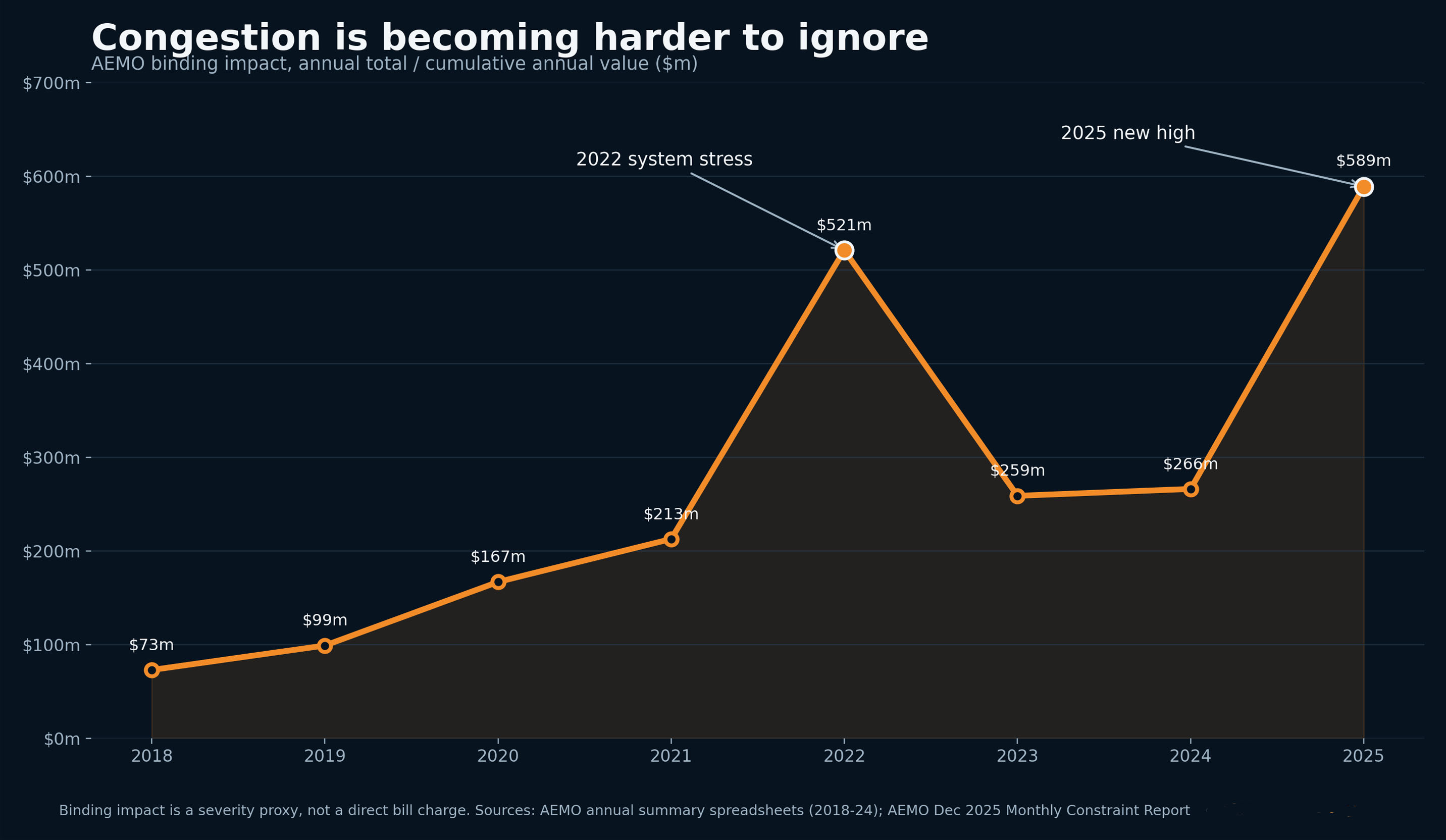

We do not eliminate those differences by averaging them. We simply push them out of sight. They reappear elsewhere, in the form of constraint costs, curtailment, volatile marginal loss factors, and increasingly blunt attempts to steer investment through administrative mechanisms. The chart below shows the increasing impact of network constraints in the National Electricity Market over time using AEMO's “binding constraint impact” as a proxy for congestion severity. When the grid cannot move electricity freely, the system has to intervene — redispatching generators, curtailing output, and managing flows manually. The underlying cost of those constraints has risen sharply, particularly during periods of system stress.

Congestion isn’t new. What’s new is how fast it’s growing — and how little of it is reflected in price.

Congestion isn’t new. What’s new is how fast it’s growing — and how little of it is reflected in price.

AEMO's binding constraint impact — a proxy for how often and how hard the network fails to move electricity freely — has risen from $73m in 2018 to $589m in 2025. That's an eight-fold increase. Even excluding the 2022 system-stress spike, the underlying trajectory is clear, and troubling. That isn't a number that shows up on a power bill, but it's the closest publicly-available measure of how often the network is overwhelmed.

When a solar farm is curtailed because the network cannot carry its output, that is a price signal trying to exist without a price. When batteries cluster in locations that are convenient rather than optimal, that is a signal that never quite made it into the market. When transmission spending rises sharply in response to congestion that could have been partially solved with better siting and coordination, that too reflects the absence of clear locational incentives.

Other markets confronted this problem earlier. Their response was not to eliminate complexity, but to expose it in a usable form. Locational marginal pricing does exactly that. It separates the price of electricity into its underlying components: the cost of producing the next unit of energy, the cost of congestion on the network, and the cost of losses as power flows across distance. The result is not a single regional average, but a set of prices that vary across the grid, reflecting real conditions in real time.

The effect of this is not academic. It changes behaviour. Storage is drawn to locations where it can relieve congestion or arbitrage meaningful spreads. Generation is incentivised to locate where its output can actually be delivered. Demand response becomes more valuable where the system is tight, and less so where it is not. Congestion, instead of being an opaque operational issue, becomes visible and, crucially, hedgeable through financial instruments. In short, money begins to align more closely with physics.

That alignment matters way more now than it did in the past. Australia is entering a phase where the marginal value of coordination is rising quickly. We have already succeeded in deploying huge volumes of solar panels, and we are now accelerating into batteries, both grid-scale and behind the meter. The next challenge is not simply to add more capacity, but to orchestrate what we already have. A system with millions of distributed devices cannot be efficiently managed with coarse signals. It requires prices that carry information about where flexibility is needed, not just when.

Australia has not ignored this debate. It has been having it, in various forms, for the better part of a decade. The AEMC's 2018 Coordination of Generation and Transmission Investment review (COGATI) opened the door explicitly, proposing a move toward locational marginal pricing supported by financial transmission rights — the same combination used in New Zealand, parts of North America, and Singapore. The reaction from much of industry was hostile. Incumbent generators feared revenue erosion, renewable developers worried about basis risk they could not yet hedge, and the political appetite for adding complexity to an already contested market was thin. By around 2021, full nodal pricing had effectively been taken off the table.

What followed was a search for something softer. The Energy Security Board, and then the AEMC, spent years developing a hybrid model: a "priority access" mechanism to provide investment-timeframe certainty, paired with a voluntary Congestion Relief Market that would let participants opt in to cost-reflective bidding when network constraints bound. The CRM was, in essence, an attempt to capture some of the operational efficiency of locational pricing without forcing it on anyone. It had genuine support; the Clean Energy Council went so far in 2023 as to declare LMP "finally dead" and the CRM the smarter path forward. Then in September 2024, the AEMC delivered its final report and recommended against implementing the hybrid model at all — including the CRM — concluding that the benefits were too uncertain to justify the complexity, and that jurisdictional schemes like Renewable Energy Zones were already doing enough of the locational signalling work. Energy Ministers accepted that recommendation.

So here we are. A decade of debate has produced neither LMP nor its compromise. The underlying problem the original COGATI review identified has, on every measure that matters, grown larger.

None of this is to suggest that locational pricing is a trivial upgrade. It is not. The complexity is real, and so are the risks. Moving from regional pricing to a nodal system introduces basis risk between locations. It requires the development of robust hedging instruments such as financial transmission rights. It complicates contracting, increases the demands on participants, and raises legitimate concerns about transition costs and political acceptability. These are not minor considerations, and they explain why Australia has been cautious. Making any major changes to our NEM, which involves five states and three regulatory bodies, is notoriously difficult.

But it is important to be clear about the alternative. Retaining the current structure does not avoid these costs; it redistributes them. Instead of explicit congestion prices, we get implicit ones embedded in losses, curtailment, and system interventions. Instead of transparent signals for investment, we rely more heavily on planning frameworks and administrative overlays. Instead of aligning incentives directly, we attempt to approximate alignment through a growing set of rules and adjustments. The system does not become simpler. It becomes opaque.

This does not mean the path forward must be binary. Full nodal pricing is one option, but it is not the only one. There is a spectrum of intermediate steps — incremental moves that can bring price closer to physical reality without requiring a wholesale redesign, and that create a pathway for participants to adapt gradually rather than abruptly.

What matters is the direction of travel. The grid is becoming more local in its constraints and more distributed in its resources. Pricing that remains coarse in the face of that evolution will increasingly struggle to coordinate outcomes efficiently.

One response has emerged outside the regulatory process altogether. Tom Walker, the former AEMC senior economist who led much of the original COGATI work, founded TxChange in 2025 to address congestion commercially rather than through rule changes. TxChange facilitates bilateral derivative contracts between counterparties exposed to congestion — sharing the value currently left on the table when renewables are curtailed. It is a clever workaround for market inefficiency but it cannot deliver the system-wide investment signals that proper locational pricing would. It is telling that the person who spent a decade trying to fix this from inside the regulator has concluded the way forward is to build a private market around the problem. When the institutional reform process stalls, markets fill the gap as best they can. That is a sign of unmet demand, not of a solved problem.

Whether through formal locational marginal pricing or through credible approximations of it, the system will need to find a way to express location in price. And that pressure is about to intensify. After two decades of flat demand, data centres are bringing load growth back — and load growth in specific places, at specific times, magnifies the cost of every signal the market fails to send.

The intermediate steps exist. Publishing shadow nodal prices in real time alongside regional prices would expose what the current system hides, without changing any settlement rules. Increasing the number of regions or pricing zones is harder, but well within the possible. None of these is the wholesale redesign that the AEMC rejected in 2024. All of them would put price closer to physics. The question is no longer whether Australia can do locational pricing — the CRM debate showed that the appetite for a softer compromise exists. The question is whether, having rejected both LMP and the CRM, the country can find the will to attempt anything at all.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Australian Energy Market Commission. (2018). Coordination of generation and transmission investment: Final report. AEMC.

Australian Energy Market Commission. (2019). Coordination of generation and transmission investment: Access reform directions paper. AEMC.

Australian Energy Market Commission. (2020). COGATI implementation: Access and charging. AEMC.

Australian Energy Market Operator. (n.d.). Congestion information resource. AEMO.

Australian Energy Market Operator. (2019). Coordination of generation and transmission investment: Access reform submission. AEMO.

Australian Energy Regulator. (2020). AEMC market review: Coordination of generation and transmission investment — implementation, access and charging. AER.

Australian Energy Market Operator. (2024). NEM constraint information: Annual summary statistics (2018–2024). AEMO. https://aemo.com.au/energy-systems/electricity/national-electricity-market-nem/system-operations/congestion-information-resource/statistical-reporting-streams

Australian Energy Market Operator. (2025). Monthly constraint report: December 2025. AEMO. https://www.aemo.com.au/energy-systems/electricity/national-electricity-market-nem/system-operations/congestion-information-resource/statistical-reporting-streams

Electricity Authority Te Mana Hiko. (2025). Geography, locational pricing and price separation. Electricity Authority.

Electric Reliability Council of Texas. (2010). 2010 state of the market report for the ERCOT wholesale electricity markets. ERCOT.

Transpower New Zealand. (2018). Market 101: Locational marginal pricing. Transpower.

TxChange website: TxChange. (2025). TxChange [Website]. https://txchange.com.au/

Wolak, F. A. (2022). Quantifying the benefits of a nodal market design in the Texas electricity market. Energy Economics.

Zuur, C. (2023, February 27). Locational marginal pricing is finally dead. Time to get smart about grid congestion. RenewEconomy. https://reneweconomy.com.au/locational-marginal-pricing-is-finally-dead-time-to-get-smart-about-grid-congestion/

Discussion

Loading comments...