Australia's battery build-out has crossed the Rubicon

Issue 02: Australia's grid-scale battery pipeline crosses 12 GW as FCAS revenue collapses and arbitrage takes over

Something changed this week in Australian energy markets. Not an individual event but a pattern. This is what inevitability looks like.

If you want to know when something stops being an energy transition narrative and becomes infrastructure, watch what happens in the financing and approvals channels—not the opinion pages.

In the space of eight days in February 2026, Australia saw a coordinated surge of storage commitments across the east coast grid:

-

NSW contracted six long‑duration batteries totaling 1.17 GW / 11.98 GWh under the Roadmap’s LTESA framework (Tender Round 6).

-

Victoria fast‑tracked approvals for 700 MW of grid batteries through its Development Facilitation Program.

-

Queensland switched on CleanCo’s 250 MW / 500 MWh Swanbank Battery on a former coal site.

-

South Australia: EnergyAustralia hit financial close on the 50 MW / five‑hour Hallett BESS beside its 235 MW gas plant.

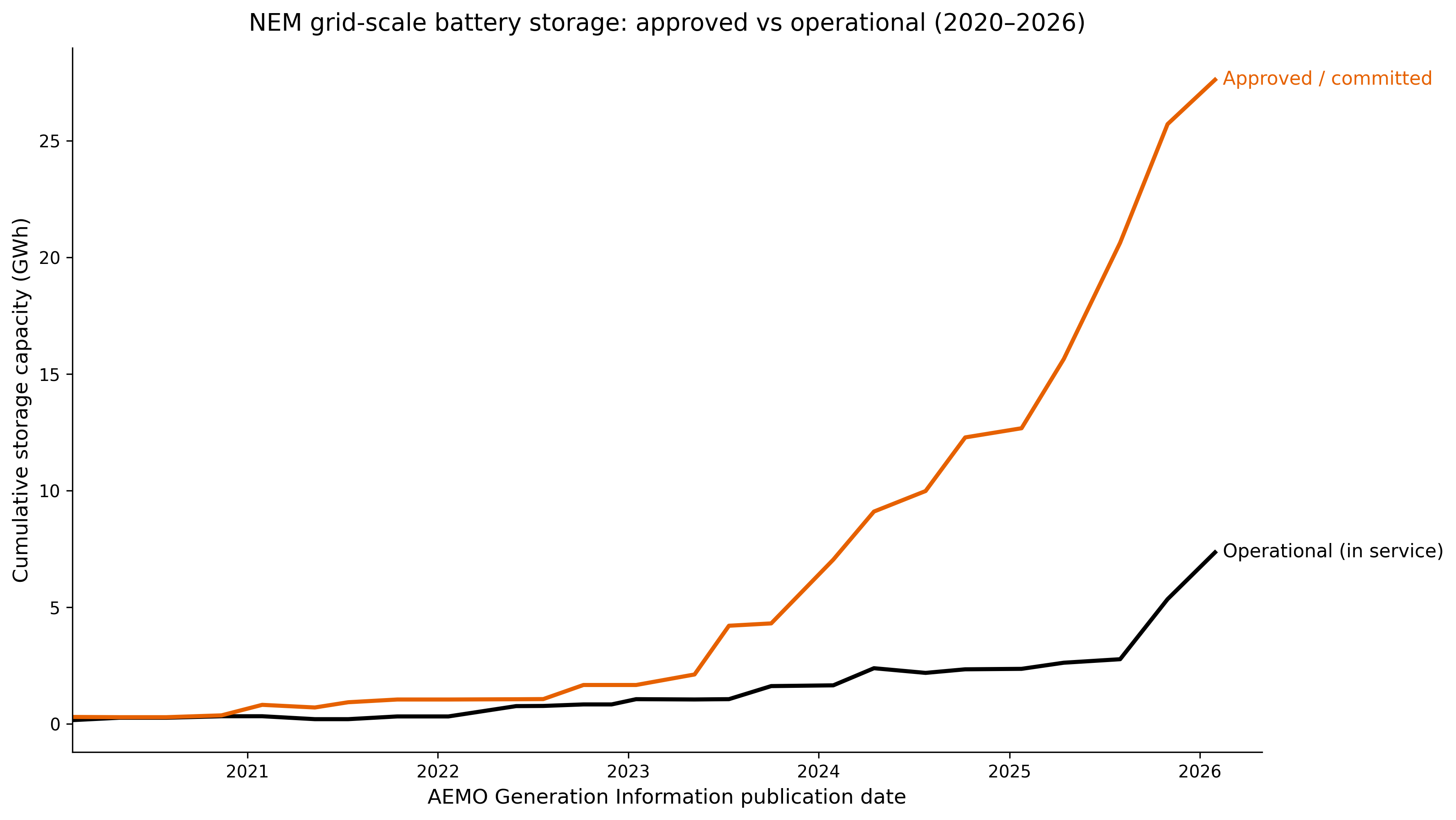

Add it up and you’re looking at north of 2 GW and ~15 GWh moving, in public view, from plan to commitment. That is not “pilot phase”. That is the system starting to re‑wire itself. That single week’s commitments amount to roughly half the entire grid-scale battery energy currently operating in the NEM.

Using AEMO’s archived NEM Generation Information files (Jan 2020 → Jan 2026), filtered Storage – Battery / Battery Storage rows and summed storage capacity (MWh).

Using AEMO’s archived NEM Generation Information files (Jan 2020 → Jan 2026), filtered Storage – Battery / Battery Storage rows and summed storage capacity (MWh).

For years, critics said grid‑scale batteries were marginal—fine for FCAS, maybe for two‑hour arbitrage, but ultimately a subsidy‑led project that collapses the moment prices get difficult. Seen in aggregate, the battery wave has been building for five years: the approved/committed pipeline has pulled well ahead of the operating fleet, and the gap has been widening. The burst of ~15 GWh listed above lands on top of that trend — which is why the “batteries are marginal” argument no longer fits the numbers.

The market has crossed a threshold: storage is no longer an adjunct to reliability. It’s becoming the core of how reliability is procured.

NSW just proved the “missing money” problem was real—and solvable

The biggest single recent proof point is New South Wales.

On 5 February, ASL announced that six new long‑duration storage projects had been contracted as the outcome of Tender 6—~1.17 GW / ~12 GWh, taking NSW’s contracted new storage capacity to 30 GWh.

The NSW Government helpfully listed the winners and sizes (in energy terms): Great Western (3,500 MWh), Bannaby (2,676 MWh), Bowmans Creek (2,414 MWh), Armidale East (1,440 MWh), Kingswood (1,080 MWh), and Ebor (870 MWh)—all due by 2030.

Here’s the part that matters: ASL’s CEO Nevenka Codevelle said the quiet part out loud—these were “eight‑hour‑plus storage projects that would not otherwise have reached financial close.”

That’s the Rubicon, right there.

For years, long‑duration storage lived in a dead zone: technically feasible, strategically valuable, but hard to finance merchant. NSW’s LTESAs did the unglamorous, essential thing: they turned reliability into something investors can underwrite. ASL explicitly frames the LDS LTESA as designed to solve the “missing money” challenge for long‑duration storage by improving bankability.

Once you fix bankability, capital doesn’t politely arrive. It arrives all at once.

Victoria attacked a different constraint: time lost in approvals

Five days later, 10 February, Victoria’s government approved two large BESS projects totaling 700 MW via the Development Facilitation Program: Atmos Renewables’ 285 MW / 1,140 MWh Heywood project near AusNet’s Heywood Terminal Station and Akaysha Energy’s 400 MW / 1,600 MWh Glenrowan project near AusNet’s Glenrowan Terminal Station.

Why this matters: Victoria’s DFP is not “support” in the subsidy sense. It’s a time machine. The government’s rationale is explicitly about accelerating critical infrastructure, with reporting that VCAT processes had delayed around 20% of projects by about two years prior to the renewable‑expansion of the program.

In other words: Victoria is removing the planning bottleneck that turns “cheaper tech” into “late delivery”. You can have all the cost declines in the world—if approvals take forever, entropy wins.

Queensland and South Australia delivered the other half of the story: execution, not theory

Then, on 13 February, two things happened that look mundane but are actually the signature of “infrastructure phase”.

CleanCo officially opened the 250 MW / 500 MWh Swanbank Battery at the former Swanbank coal power station site in Ipswich, built with Tesla Megapacks, funded through Queensland’s Renewable Energy and Hydrogen Jobs Fund (AU$330 million), and explicitly framed as repurposing retired coal infrastructure into a “clean energy hub.”

Also on 13 February, EnergyAustralia announced financial close for its Hallett BESS: 50 MW with five hours of storage in stage one, built beside its existing Hallett gas‑fired power station, with planning approval in place for an additional 150 MW (total site ambition 200 MW). EnergyAustralia highlights that the battery will connect through existing equipment, minimising new transmission works, with commercial operations expected mid‑2027.

These aren’t rhetorical projects. They’re funded, contracted, and moving into delivery. That’s the difference between “transition commentary” and “transition hardware.”

The geography is the tell: the grid is being rebuilt from its old bones

Look at what links these projects: they cluster around existing nodes.

A battery beside a gas plant, using existing connection equipment.

A battery on a coal site, leveraging established transmission connections (and a new 275 kV substation feeding into the same grid reality).

This is not symbolism. It’s the market doing the rational thing: treating grid access like a scarce asset and turning yesterday’s thermal sites into today’s transition hubs. The incumbents built the ports; the new system is sailing in through them.

“Baseload territory” is becoming “flexibility territory”—not because anyone changed their mind, but because the most valuable thing at a constrained node is increasingly the ability to shape energy, not just generate it.

Costs are falling, but this week wasn’t about costs

Yes, storage economics keep improving. The price curve is bending hard enough that analysts have been comfortable saying things like “average LFP cell prices were just under $60/kWh in 2024.”

But: this week’s story isn’t chemistry. It’s the fact that Australia is now building the scaffolding that turns falling costs into built assets—contracts that underwrite reliability, and approval mechanisms that compress timelines.

Technology makes it possible. Market design makes it financeable. Planning makes it buildable. That triad is what “crossing the Rubicon” actually looks like.

The real question has moved—again

The debate is no longer whether grid‑scale batteries are viable.

The debate is now:

-

whether deployment outruns coal’s retirement schedule, and

-

whether market rules evolve fast enough to value flexibility (and essential system services) as a first‑class product rather than an afterthought.

Because here’s the uncomfortable truth for the remaining skeptics: every banked long‑duration contract reduces the political and financial room for thermal life‑support. Every medium‑duration battery at a strategic node eats into the scarcity story that peakers rely on. Every repurposed coal site becomes a reminder that “stranded asset” is not a metaphor—it’s an accounting category waiting for a timestamp.

The centre of gravity is shifting. Not rhetorically. Financially.

And once capital recognises that storage has moved from experiment to repeatable infrastructure, it does not trickle in. It floods.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

SOURCES

AEMO Services Limited. (2026, February 4). Six new battery energy projects secured in state’s largest ever tender for long duration storage. https://asl.org.au/news/media-release/260205-asl-nsw-roadmap-tender-6-outcomes-announced

AEMO Services Limited. (n.d.). NSW electricity infrastructure tenders: Market briefing note on outcomes of Tender Round 6 for long duration storage infrastructure [PDF]. Retrieved February 21, 2026, from https://asl.org.au/-/media/services/files/tender-round-6/260130-nsw-roadmap-tender-round-6-market-briefing-note.pdf

Premier of Victoria. (2026, February 9). Fast-tracking cleaner and cheaper energy. https://www.premier.vic.gov.au/fast-tracking-cleaner-and-cheaper-energy-0

Atmos Renewables. (n.d.). Heywood battery energy storage system (BESS). Retrieved February 21, 2026, from https://atmosrenewables.com.au/project/heywood-bess/

Akaysha Energy. (n.d.). Glenrowan BESS. Retrieved February 21, 2026, from https://akayshaenergy.com/projects/glenrowan-bess

Queensland Government. (2026, February 5). Battery milestone strengthens Queensland grid and powers Energy Roadmap. https://statements.qld.gov.au/statements/104427

CleanCo Queensland. (2026, February 5). Battery milestone strengthens Queensland grid and powers Energy Roadmap. https://cleancoqueensland.com.au/battery-milestone-strengthens-queensland-grid-and-powers-energy-roadmap/

Queensland Government. (2024, February 19). Construction starts on one of Queensland’s biggest batteries [Joint statement]. https://statements.qld.gov.au/statements/99735

EnergyAustralia. (2026, February 13). Hallett battery project reaches major milestone in South Australia. https://www.energyaustralia.com.au/about-us/media/news/hallett-battery-project-reaches-major-milestone-south-australia

FURTHER READING

Australian Energy Regulator. (n.d.). LTESA tender rules. Retrieved February 21, 2026, from https://www.aer.gov.au/about/strategic-initiatives/renewable-energy-zones/our-role-nsw-rez/ltesa-tender-rules

AEMO Services Limited. (2023). Tender Round 2—Firming infrastructure: Market briefing note [PDF]. https://asl.org.au/-/media/services/files/publications/market-briefing-series/234415-tender-round-2-market-briefing-note-final-002.pdf

Australian Energy Market Operator. (2024, June 26). 2024 Integrated System Plan (ISP). https://aemo.com.au/energy-systems/major-publications/integrated-system-plan-isp/2024-integrated-system-plan-isp

Premier of Victoria. (2024, March 14). Faster approvals for more jobs and lower power prices [Media release]. https://www.premier.vic.gov.au/sites/default/files/2024-03/240314-Faster-Approvals-For-More-Jobs-And-Lower-Power-Prices.pdf

Jayanthan, S. (2025, January 8). Where are EV battery prices headed in 2025 and beyond? S&P Global Mobility. https://www.spglobal.com/automotive-insights/en/blogs/2025/01/where-are-ev-battery-prices-headed-in-2025-and-beyond

Our World in Data. (2025, December 2). Lithium-ion battery cell prices by chemistry [Dataset]. https://ourworldindata.org/grapher/average-battery-cell-price

Discussion

Loading comments...