Grid stability has some important new tools

Issue 12: Distributed energy resources increasingly keep the system stable. Time they were better recognised.

In California, the physical system that keeps the grid running has already changed. The market is still catching up. A new proposal to give distributed energy resources clearer pathways into the system is an important part of that.

California Senator Josh Becker has introduced legislation that would require regulators to create clearer pathways for distributed energy resources to participate in the state’s resource adequacy framework. Home batteries, electric vehicles, rooftop solar with storage: all would gain more systematic access to the mechanism that ensures grid reliability. This isn’t regulatory tinkering; it’s an admission that the old model of grid adequacy, built around centralised generation, no longer matches the reality of where reliability actually comes from.

California’s resource adequacy system isn’t a traditional centrally cleared capacity market. It’s a regulatory framework that requires load-serving entities to demonstrate they have sufficient "qualifying capacity" available to meet peak demand plus a safety margin, in the right locations, at the right times. Generators, and other qualifying resources, are compensated for being available, not just for producing energy. It is, in effect, an insurance policy against blackouts, and it has traditionally been dominated by large-scale resources: gas peakers, hydroelectric stations, imports, and contracted demand response. The logic was straightforward. Big assets are visible, controllable, and their availability can be measured with reasonable certainty.

But that logic was forged in an era when the grid was essentially a one-way street, with generation at one end and consumption at the other.

That era is ending. California now has well over a million rooftop solar systems installed. Battery deployments are accelerating across residential and commercial properties. Electric vehicle adoption is surging, and each EV represents a mobile battery that spends most of its life parked. These are no longer fringe technologies; they are becoming part of the physical fabric of the grid, already contributing to system stability through a mix of programmes, pilots, and emerging market participation pathways.

What’s missing isn’t technology; it’s alignment. Distributed resources can already participate in parts of California’s market structure, but their pathways into the reliability framework remain narrow, complex, and poorly scaled relative to the resource base that now exists.

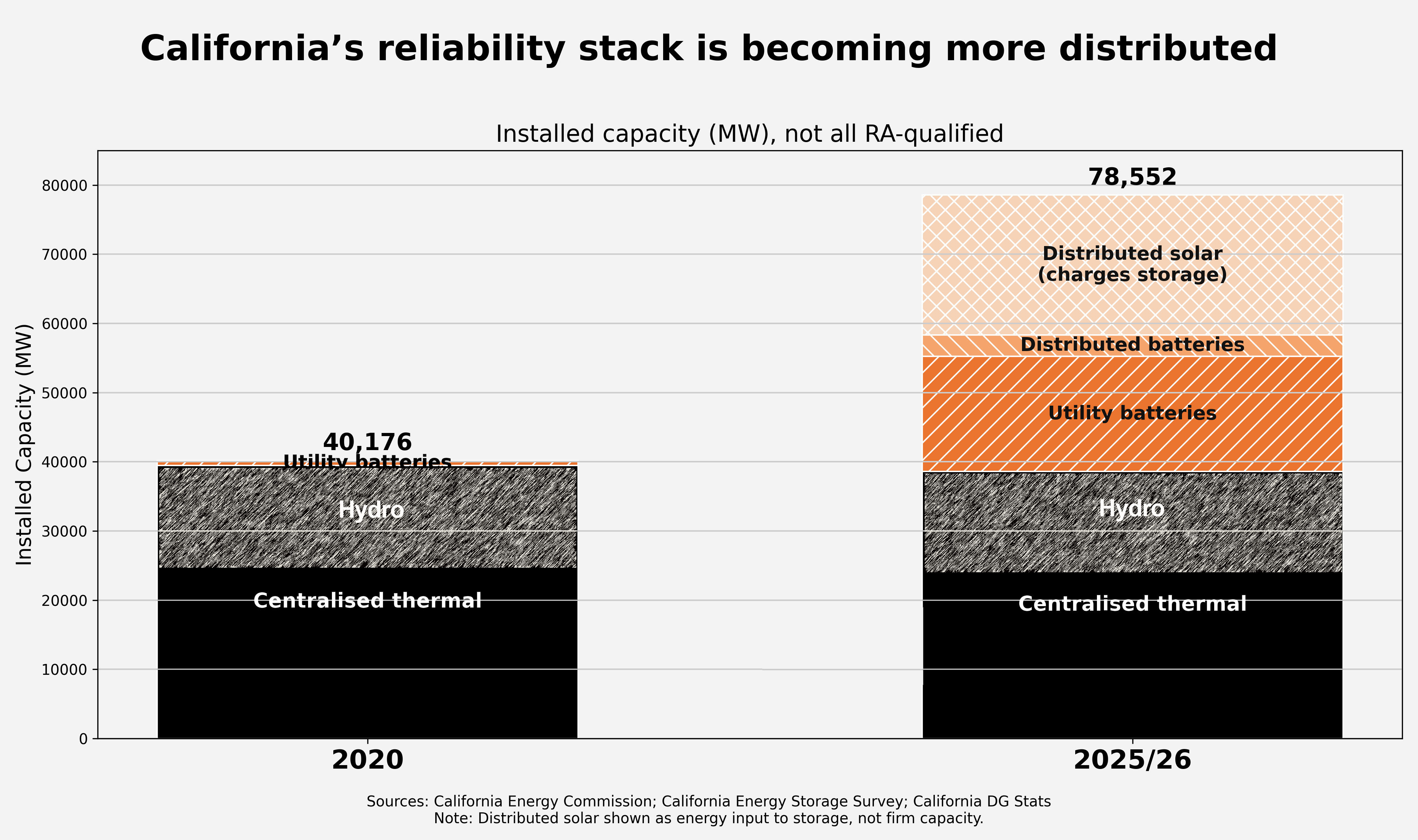

The shift is already visible in the physical system itself.

As the composition of capacity has changed, so too has the source of reliability, even if the framework that recognises it has not. Rooftop solar is included in the above chart because it is a large and growing part of the physical system that shapes when and how reliability is delivered, even if it is not itself firm capacity. In practice, it charges distributed and grid-scale batteries and reduces daytime load, and it underpins the storage that is counted as reliability.

Australia’s National Electricity Market offers a preview of where this heads. Rooftop solar has reshaped daytime demand. Battery storage is being deployed at both grid scale and, increasingly, at household level. AEMO’s NEM Virtual Power Plant Demonstrations, launched in 2019 with ARENA support, showed that aggregated consumer devices such as household batteries can be coordinated to respond to wholesale price signals and deliver services including grid frequency support (FCAS) and local network support.

The system did not set out to become distributed; it became distributed because the economics made it inevitable.

California’s proposal formalises what is already happening informally. Distributed energy resources respond to price signals. They provide capacity during peak periods. They reduce strain on transmission infrastructure by generating and storing energy close to where it is consumed. What they have lacked is consistent, scalable recognition within the framework that values reliability.

The technical challenges are real, but they are not fundamental. Aggregating thousands of small batteries into a dispatchable resource requires software, telemetry, and coordination. Measuring the availability of an EV fleet is harder than checking whether a gas turbine is online. Baselines, performance verification, and aggregation rules all matter. But these are engineering and market design problems, not barriers to entry. Virtual power plant operators have already demonstrated that distributed assets can be orchestrated to behave, from the system’s perspective, like a single, reliable resource.

Opening the resource adequacy framework to distributed resources doesn’t just expand the pool of capacity. It changes the economics of investment. If a household battery can earn revenue from both energy arbitrage and reliability services, the payback period shortens. More batteries get installed. The system becomes more resilient by distributing capability across millions of endpoints rather than building another centralised plant. This is how modern infrastructure scales by coordinating many small components more effectively.

There’s another important change happening here. Centralised generation operates on top-down dispatch and control. Distributed resources operate on bottom-up orchestration and incentives. Create the right price signal, and thousands of devices respond in aggregate. It is a different architecture: less hierarchical and more emergent. California’s legislation doesn’t create that shift; it acknowledges that it has already happened.

This isn’t progressive policy or climate ambition dressed up as market reform. It’s infrastructure economics catching up with physical reality. The grid is already distributed. The question is whether market structures evolve to reflect that, or whether they continue to reflect a system that no longer exists.

Markets work when participants can compete on comparable terms. Resource adequacy isn’t about technology type or fuel source. It’s about ensuring capacity is available when and where it’s needed. If distributed resources can provide that capacity, reliably and at scale, then the framework needs to recognise them accordingly.

Senator Becker’s bill doesn’t mandate outcomes. It pushes toward access. The rest is a question of implementation, and of whether institutions can adapt as quickly as the system they are meant to govern.

The direction is already clear. Reliability is becoming more distributed, more software-mediated, and more dependent on coordination at the edge of the grid.

The real question is whether market design keeps up.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Australian Energy Market Operator. (2021, September 17). AEMO shares fourth and final VPP knowledge sharing report ahead of trial conclusion.

Australian Energy Market Operator. (2021). NEM virtual power plant (VPP) demonstrations: Knowledge sharing report 4.

Australian Energy Market Operator. (n.d.). Virtual power plant (VPP) demonstrations. Retrieved April 1, 2026

California Distributed Generation Statistics. (n.d.). California leads the nation in distributed generation. Retrieved April 1, 2026, from

California Energy Commission. (n.d.). California energy storage system survey. Retrieved April 1, 2026, from

California Public Utilities Commission. (n.d.). Resource adequacy homepage. Retrieved April 1, 2026, from

California Public Utilities Commission. (2025, August). 2023 resource adequacy report.

California Public Utilities Commission. (2026). 2026 resource adequacy and slice of day guide.

Kennedy, R. (2026, March 27). California bill targets DER access to resource adequacy market. pv magazine USA.

Office of Senator Josh Becker. (2026, March 24). Becker introduces SB 913 to make better use of customer-owned clean energy resources.

Discussion

Loading comments...