The grid squeeze: Our grid Is not full, but we keep building it.

Issue 09: How demand flexibility and distributed batteries could defer $100 billion in grid infrastructure

A coalition of US tech giants claims using our existing electricity networks better could save $100 billion in grid infrastructure costs. They are probably right. In Australia we are still building more networks to carry less electricity.

A coalition led by Google, Tesla and Carrier has put forward a simple proposition: use the grid more efficiently and the United States could save consumers more than US$100 billion over the next decade. It is an attractive message, especially for large new loads such as data centres, because it promises faster access to power without waiting for every line and substation to be rebuilt. The Brattle report behind the claim is more nuanced than the slogan. It talks about storage, demand flexibility, energy efficiency, better tariffs, flexible interconnection and smarter system planning, not a magic trick that makes wires optional.

That distinction matters. Cheap batteries have changed the economics of the grid. They let electricity be moved from one moment to another, which means a storage system can charge when the network is quiet and discharge when it is stressed. In the right circumstances, that can defer a conventional upgrade. But that is not the same as saying batteries can broadly replace networks. There is a difference between operational optimisation, which means getting more out of assets already in place, and capital substitution, which means avoiding new investment altogether. The first is real and increasingly important. The second is much narrower than many of its advocates imply.

Storage is strongest where the problem is local, short-lived and highly peaky. A feeder that runs hot for a few summer evenings is a good candidate. A substation that is only tight during short demand spikes is another. In those cases, batteries and demand response, meaning customers being paid to reduce or shift usage when the grid is tight, can stand in for steel and concrete. The bulk transmission system is different. It is built to move energy across geography, manage uncertainty and provide resilience. That is why the honest version of the US proposition is not that batteries replace wires. It is that batteries can replace some wires, some of the time.

The Australian question is therefore not whether better utilisation matters. It plainly does. The real question is why a country with world-leading rooftop solar, rapidly rising battery adoption and sophisticated market institutions has done such a poor job of using its existing network better.

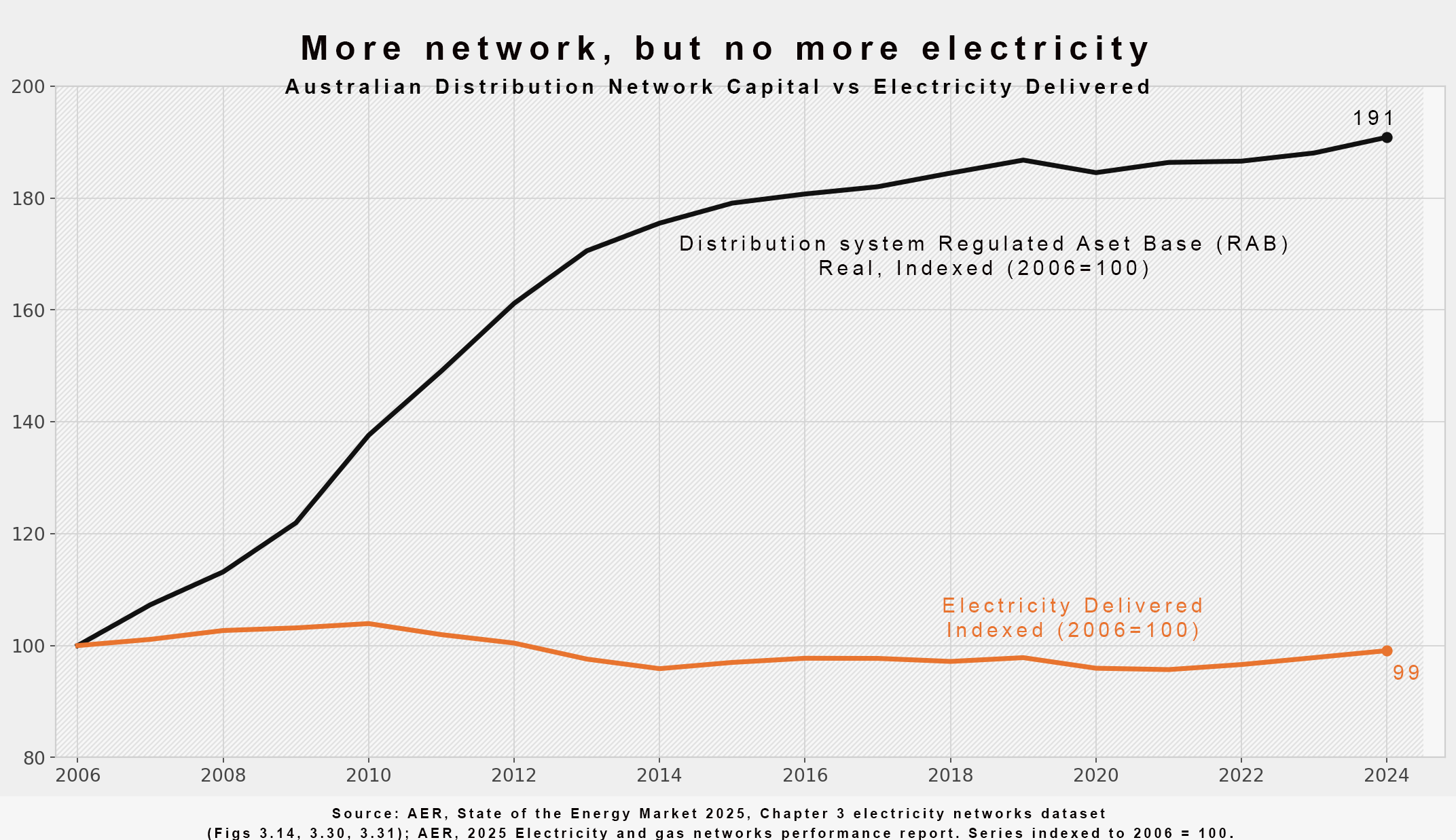

The facts are uncomfortable. On the Australian Energy Regulator’s Chapter 3 data, capital invested in the distribution grid, the local poles, wires, transformers and substations that serve homes and businesses, has almost doubled since 2006, while electricity delivered through that grid has barely moved.

It is important to be clear about what that flat electricity number does and does not mean. It does not mean Australian households and businesses have stood still. In part, it reflects more of the energy story moving behind the meter. The Australian Energy Regulator says average demand has declined since 2006, driven in part by improved energy efficiency and increased self-consumption of solar photovoltaic, or solar PV, systems. It also notes that rooftop solar uptake has grown exponentially and that battery storage is increasingly being used to store that energy. In other words, flat grid-delivered electricity is partly what a decentralising system looks like. More electricity is being produced and used on rooftops and in homes, rather than always flowing through the traditional grid in the old one-way pattern.

That makes the Australian result look worse, not better. A system with more rooftop solar and more home batteries should have pushed the industry much harder toward orchestration, smarter tariffs and more selective capital spending. Instead, the legacy logic of the network remains dominant. The Australian Energy Regulator is blunt about the mechanism: capital expenditure is largely driven by maximum demand, yet the assets built to meet that maximum demand may only be needed for around 0.01% of the year. Its own report says such assets may sit idle or underused for longer periods, and that this shows up in poor asset-usage rates and lower utilisation. There was a lift in 2024, when the regulator’s maximum-demand utilisation metric rose to 45%, the highest since 2013, but that is hardly a victory lap. It is a reminder of how weak the preceding decade was.

One part of the problem is that our price system remains far too blunt. Australia’s National Electricity Market, or NEM, is the wholesale electricity market across the eastern states and territories. It is fast, with prices set every five minutes, but geographically coarse. In the wholesale market, because Bondi and Bourke are both inside the same NEM region, they have the same regional spot price at a given moment even if local network conditions are very different. The Australian Energy Market Commission has argued for years that this region-wide pricing model weakens locational signals and hides the true economics of congestion within a region. It has also argued that consumers currently bear too much of the risk when transmission investment turns out to be wrong.

That pricing bluntness flows into the rest of the system. Distribution network service providers, or DNSPs, are the regulated monopolies that run the local distribution grid. They recover revenue through a regulatory framework that is built around a regulated asset base, or RAB, which is the value of the capital stock on which they earn a regulated return. In theory, the system has room for demand management, non-network solutions and experimentation. In practice, the financial engine still runs on capital. The rhetoric says flexibility. The cashflows still say build.

That is why the RAB story matters so much. It is not just a technical metric. It is a record of what the system has chosen to reward. When the distribution RAB nearly doubles while delivered electricity barely moves, the right response is not to shrug and say the transition is complicated. Of course it is complicated. The right response is to say that the incentive structure has been badly misaligned with the physical reality of the grid.

The Australian Government’s 2025 National Electricity Market Wholesale Market Settings Review addresses this issue. While it does not use the language of “overbuild,” it clearly recognises that parts of Australia’s distribution network are under-utilised, drawing on Australian Energy Regulator evidence that some assets are used infrequently and that customers may be paying for capacity they rarely need. It links this directly to tariff design, noting that current network pricing can be too blunt to reflect when and where capacity is available, and can therefore discourage efficient use of existing infrastructure and consumer resources such as batteries and demand response. Importantly, the Review frames this not as a failure of engineering, but as a market design problem, recommending sharper price signals and better integration of distributed energy to improve utilisation and avoid inefficient future investment.

To be fair, there are signs of progress. Ausgrid’s Project Edith is exactly the kind of experiment the sector should have mainstreamed by now. Ausgrid says the project has shown how dynamic pricing can help solar, batteries and electric vehicles participate in energy markets while staying within distribution network capacity limits, and that an end-to-end dynamic network pricing service can be built on existing systems. CitiPower and Powercor’s use of the Piclo flexibility marketplace is another move in the right direction. Powercor says the platform is intended to make local constraints visible and help third parties provide non-network solutions that defer, reduce or remove the need for network investment. Piclo says the Victorian partnership is about opening more of the network’s constraints to build a flexibility market. Those developments are encouraging. They are also revealing. After years of rooftop solar growth, better use of the network is still something Australia mostly does in trials and targeted procurements, not as the normal operating model.

And that brings us back to incentives. The problem is not that nobody in the industry understands the opportunity. They do. The problem is that the regulatory system does not yet make better utilisation the default commercial path. It does not consistently reward a DNSP for solving a local constraint with orchestration rather than augmentation. It does not expose consumers and distributed resources to prices that clearly reflect where the grid is tight and where it is slack. It does not make non-network solutions feel like the mainstream choice.

The Australian story, then, is not that the grid is full. It is that our institutions were built for a one-way system and still pay people more reliably for expanding it than for orchestrating it. Rooftop solar and home batteries have made that mismatch impossible to ignore. They have changed the physical character of the grid, but not yet the economic logic that governs it.

The idea that better use of the grid can unlock major value is sound. The American debate is useful because it forces that point into the open. But in Australia the more urgent lesson is closer to home. We do not mainly have a hardware problem. We have a coordination problem, and our answer to coordination problems has too often been capital.

Until that changes, Australia will keep responding to a two-way, flexible, increasingly distributed electricity system with the instincts of a one-way network builder. And consumers will keep paying for the gap.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

AER, State of the Energy Market 2025 (Ch.3 + data) https://www.aer.gov.au/publications/reports/performance/state-energy-market-2025

AER, Electricity & Gas Networks Performance Report 2025 https://www.aer.gov.au/publications/reports/performance/2025-electricity-and-gas-networks-performance-report

Brattle, The Untapped Grid (2026) https://www.brattle.com/insights-events/publications/the-untapped-grid-how-a-better-utilized-power-system-can-improve-energy-affordability/

AEMC, CoGATI Final Report (2018)

AEMC, CoGATI Directions Paper (2019)

Finncorn, Post-2025 Market Design submission (2021)

Finncorn, Transmission Access Reform submission (2022)

Ausgrid, Project Edith https://www.ausgrid.com.au/About-Us/Future-Grid/Project-Edith

Powercor / CitiPower, Non-network opportunities (Piclo) https://www.powercor.com.au/network-planning-and-projects/non-network-opportunities/

Piclo, Energy flexibility marketplace https://www.piclo.energy/

Discussion

Loading comments...