The Forty-Year Bill

Issue #20: Why the network slice of your electricity bill is slow to fall, quick to grow, and dangerous to ignore.

Electricity bills have two clocks: fast-moving energy prices and slow-moving network costs. Australia’s regulated network assets have nearly doubled in 20 years, and electrification risks adding more forty-year infrastructure to bills. The goal is not to stop building, but to ensure customer-owned flexibility can compete with copper before the anaconda tightens. Disclosure: I am working on a venture in this field. Details at the end.

Tick. Tock.

Two clocks tick inside your electricity bill, and most people watch the wrong one. The energy clock is fast and loud: spiking on hot evenings, collapsing at midday, sometimes going negative. When solar and wind push wholesale prices down, this is the clock that can fall. We read about negative electricity prices in the media and then wonder why the bill still feels so heavy.

The second clock, the network clock, is slower. It is the cost of the poles, wires, substations and transformers, built as long-lived assets and recovered through regulated charges over decades. It is known as the Regulated Asset Base (or the RAB). It can fall, and occasionally has, but only through slow regulatory machinery. Cheap lunchtime energy does not make a transformer cheaper. It does not unwind yesterday’s capital program. It does not dissolve an approved asset base. The network clock is moved by regulatory decisions, depreciation, inflation, rates of return and new investment, not directly by afternoons of abundant solar.

For most of the grid's history the two clocks tracked each other. That relationship has broken, risking a rising floor under everyone's electricity bills, whatever the cost of energy.

Gold-plating and the memory of the 2000s

Australia has been here before.

Between the mid-2000s and mid-2010s, parts of the electricity network were heavily overbuilt. Reliability standards tightened, demand forecasts were too high, regulatory settings encouraged capital expenditure, and governments wanted to avoid blackouts. The result was a wave of network investment that customers are still paying for.

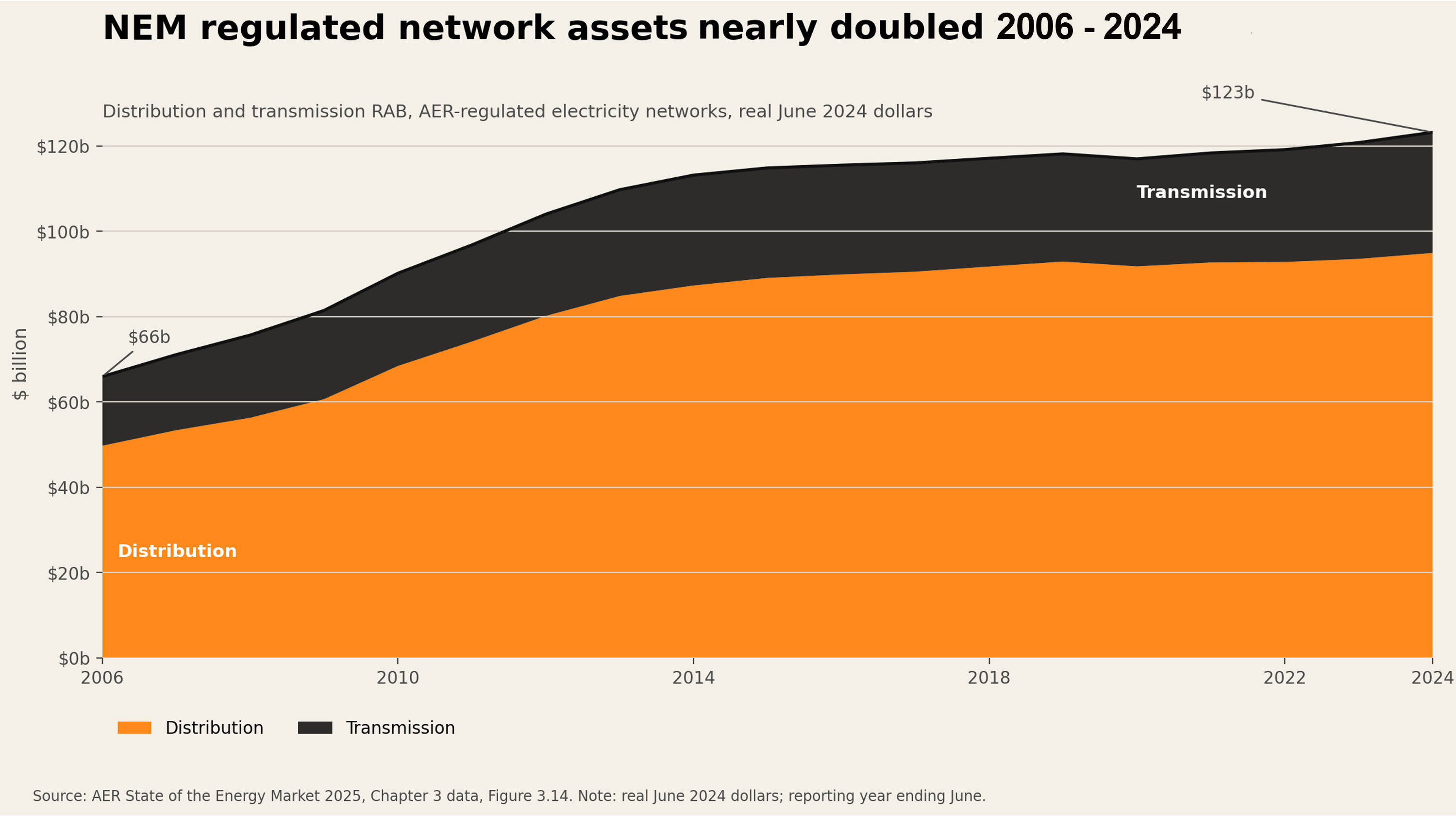

The Grattan Institute’s Down to the Wire found that the value of the National Electricity Market’s power grid grew from around $50 billion in 2005 to about $90 billion by 2016, measured in 2017 dollars and excluding interconnectors. The AER series shown in the chart above is expressed in real June 2024 dollars, which is why the numbers appear higher. The story is the same: network assets rose very sharply through the gold-plating period, and Grattan estimated that up to $20 billion of that investment was excessive, mostly in New South Wales and Queensland.

That was not a failure of the system. It was a failure of design. The machine did what it had been designed to do: forecast demand, set reliability standards, approve investment, add assets to the RAB, and recover the cost from customers. The design produced the result. With the benefit of hindsight, that design assumed demand growth that was too high, largely because it did not anticipate the huge growth of rooftop solar and changing demand patterns.

IEEFA has since argued that economic regulation of distribution networks remains a major driver of electricity bills and has not consistently delivered efficient distribution network costs.

The lesson is not that networks are bad. The lesson is that regulated network investment needs constant discipline because the consequences are slow, durable and hard to unwind.

Why using less network can make the network dearer

There is a second trap inside the network clock.

When households install rooftop solar, batteries and efficient appliances, buy fewer kilowatt-hours from the grid. That is good for them. It is good for emissions. It is good for the system, particularly if their devices are coordinated well.

But the existing network asset base does not shrink just because customers buy fewer kilowatt-hours. The poles are still there. The transformers are still there. The regulated revenue requirement still has to be recovered. If fewer units of electricity are delivered through the shared network, then more of the fixed network cost has to be recovered from each unit, or through higher fixed and demand-based charges.

This is one reason electricity bills can feel unfair in the rooftop solar era.

A household with a good roof, capital and a battery can reduce its exposure to the shared system. A renter, apartment dweller or low-income household may not have the same option. Yet they still help pay for the shared network. If the system is badly designed, the people least able to leave the network can be left carrying more of its long-lived costs.

That is not an argument against rooftop solar or home batteries. Far from it. It is an argument for better tariff design, better network planning and better ways for customer-owned assets to help the shared system rather than simply escape from it.

Why This Matters Even More Now

The RAB matters because Australia is in the midst of enormous electricity infrastructure decisions.

Coal is retiring. Renewable energy zones are being built. Transmission projects are moving forward. Distribution networks are preparing for more volatile local flows driven by rooftop solar, EVs and electrification.

A major transmission build is still underway: EnergyConnect, HumeLink, VNI West, Marinus and QNI upgrades. AEMO’s 2024 ISP put the required build at close to 10,000 km and around $16 billion, while the Draft 2026 ISP has revised the optimal path to around 6,000 km and $9 billion of transmission investment. Either way, AEMO’s case is that this transmission largely pays for itself and lowers total system costs. That is not my target here.

The sharper problem is closer to home. Electrification is moving into the street: EVs, heat pumps, induction cooking, electric hot water, batteries and even more rooftop solar. Some homes can partially self-supply. Many cannot. Apartments, renters and shaded homes are still tied more tightly to the shared system. As local demand and local exports become more volatile, distribution networks will need more capacity unless they gain better tools. The real target is distribution capex which might be deferrable: the feeder upgrade, the transformer replacement, the local reinforcement that customer-owned batteries and flexible demand might help avoid.

Data centres can help, but they are not a panacea. They are one of the first major new sources of load growth in years, and in the right places they may help spread the cost of upstream transmission. But they are geographically concentrated. A data centre does little for a residential low-voltage street where EV charging, heat pumps and evening peaks are forcing a transformer upgrade.

Some network investment is necessary. Some may be avoidable. Some may be better replaced by intelligence, coordinated home storage and flexible demand.

So the story is not “stop building.” It is that we have a machine too ready to turn local problems into forty-year assets, recovered through charges that do not automatically shrink when energy gets cheap, and too easily reallocated onto those least able to escape.

Left alone, that machine becomes the anaconda of electrification: not dramatic enough to notice at first, but powerful enough to squeeze the promise out of the whole transition.

New to this topic? See these Battling Entropy Primers and Posts to get you up to speed:

Network Charges and the RAB 101 (This is the key explainer for how the "second clock" system works)

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Australian Energy Market Commission. (n.d.). National Electricity Rules: Clause 6.5.1 — Regulatory asset base. AEMC Energy Rules.

Australian Energy Market Operator. (2024). 2024 Integrated System Plan: Roadmap for the energy transition.

Australian Energy Market Operator. (2025). Draft 2026 Integrated System Plan: Overview.

Australian Energy Regulator. (2025). State of the energy market 2025.

Australian Energy Regulator. (2025). State of the energy market 2025: Chapter 3 — Electricity networks.

Australian Energy Regulator. (2025). State of the energy market 2025: Data — Chapter 3, Electricity networks.

Grattan Institute. (2018). Down to the wire: A sustainable electricity network for Australia.

Institute for Energy Economics and Financial Analysis. (2024). Reforming the economic regulation of Australian electricity distribution networks.

Kuiper, G. (2024). Reforming the economic regulation of Australian electricity distribution networks. Institute for Energy Economics and Financial Analysis.

Ferguson, Tony (2026). The Forty-Year Bill. Renew Economy, 10 June 2026.

Wood, T., Blowers, D., & Griffiths, K. (2018). Down to the wire: A sustainable electricity network for Australia. Grattan Institute.

Discussion

Loading comments...