Do Not Disturb

Issue 18: The battery fleet nobody can call

Australia is building a vast home-battery fleet. Those batteries help their owners a lot. They could also be of great help to the grid (the physical system, not just the market). Using batteries to provide network flexibility rather than building more poles and wires could slow the growth of the distribution network and reduce consumer bills. But that isn't happening. The problem is not that the batteries can't do the job. It is that the grid cannot reach the right ones, on the right street, at the right time. Disclosure: I am working on a venture in this field. Details at the end.

From a distance, the Australian home-battery rollout looks like the final piece of the energy transition slotting into place. Rooftop solar created the midday surplus. Home batteries can shift some of that energy into the evening peak. Electric vehicles will add a much larger and more complex storage layer over time. The hardware is arriving. What is missing is coordination.

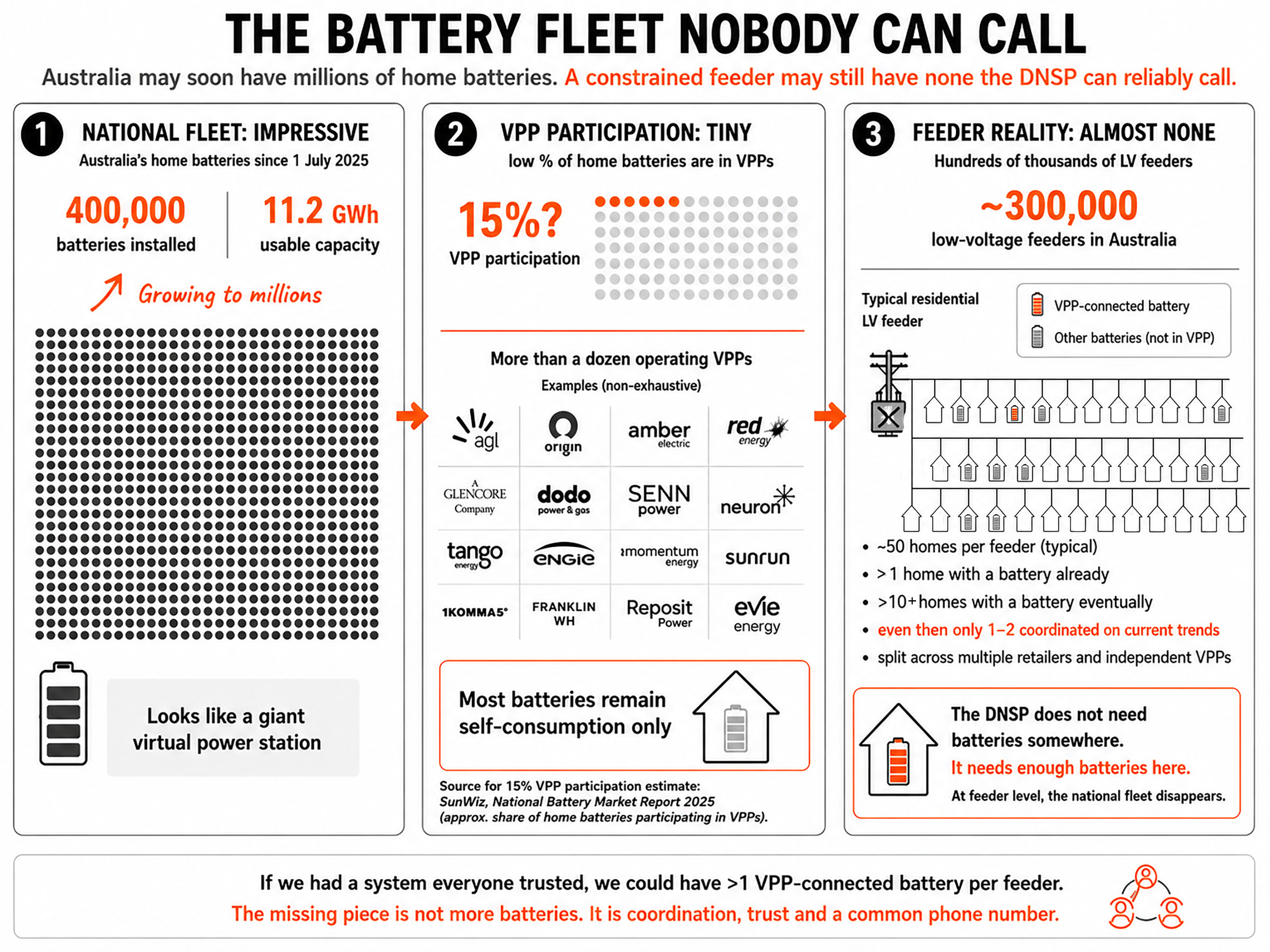

A national fleet of home batteries does not automatically solve a local network problem. Hundreds of thousands of batteries across the country can coexist with a particular low-voltage feeder that, at 6.30 pm on a hot evening, has no dependable pool of batteries the local network can actually call. That is not a contradiction. It is the difference between capacity and coordination.

In electricity, flexibility means the ability to change when power is consumed, generated, stored or exported in response to what the grid needs. A battery is flexible because it can charge at lunch and discharge in the evening. An EV charger is flexible if it can wait an hour without inconveniencing the driver. A hot water system is flexible if it can heat when solar is abundant rather than when the street is already under stress. Even an air-conditioner can provide a little flexibility if it can pre-cool a house or ease back briefly at the right moment.

The important point is timing. A kilowatt-hour used at noon and a kilowatt-hour used at 6 pm are not the same to the grid. Nor are two batteries the same if one is on a constrained feeder and the other is twenty kilometres away. Flexibility is valuable because it can turn “build more network” into “use the existing network more intelligently.”

The old integrated utility, whatever its faults, had one structural advantage that is easy to overlook. When a single organisation controlled both the network and the customer relationship, it could see the physical constraint and the customer assets in the same frame. It knew which homes sat on which feeder, what equipment was connected, and whether a battery or demand response program might be cheaper than upgrading the transformer. Coordination was simpler because the maps aligned inside one institution.

Australia deliberately chose a different model. We separated networks from retail, created competitive retailers, and built the NEM around regional, generally state-wide, wholesale prices. That architecture delivered genuine benefits in competition and innovation. It also created a persistent coordination gap. A DNSP sees the physical feeder and its constraints. A retailer sees the customer account. An aggregator sees its enrolled portfolio. The transformer does not care who sends the bill. The physical problem sits at the feeder level, but the commercial relationships are organised around accounts, portfolios and programs. When customers were passive loads, this separation was manageable. Once customer-owned batteries and flexible devices sit behind the meter, the misalignment becomes material.

Retailers and aggregators naturally optimise across portfolios. Networks must manage physical constraints on specific streets. These are both legitimate perspectives, but they are not the same object. A retailer can run a large VPP across an entire state and still have almost no useful concentration of batteries on one constrained feeder. Another retailer might have two batteries on that feeder, an aggregator one more, and the rest may be self-consumption-only devices invisible to any coordinated process. At national level the battery numbers look impressive. At feeder level they largely disappear.

Virtual power plants were the obvious first response to this challenge. They aggregate small devices and make them visible to larger markets. Most VPPs, however, are organised around a retailer, an aggregator or a device platform rather than around the low-voltage feeder. A retailer can use a VPP to reduce exposure to high wholesale prices. An aggregator can bid into frequency services. Neither is primarily designed to give a DNSP dependable response on one specific street for a few hours on a few days. Low overall VPP participation makes the problem worse. When only a small share of batteries is enrolled, and that share is fragmented across multiple operators, the chance of any single operator having enough batteries on the constrained feeder becomes low.

Australia is not ignoring the issue. Several serious projects are already testing better interfaces between customer devices and the distribution network. SA Power Networks’ Flexible Exports program replaces blunt static export limits with dynamic envelopes that reflect real-time network conditions. Ausgrid’s Project Edith has been trialling dynamic network pricing for solar, batteries and flexible load. CitiPower and Powercor have partnered with Piclo to create a flexibility marketplace that lets DNSPs procure non-network solutions more formally. Project EDGE, led by AEMO with AusNet and Mondo, demonstrated that price-responsive DER coordination across wholesale and local network services is technically feasible.

These initiatives show the system learning to ask better questions about location, timing and value. They are genuine progress. Yet they remain incomplete. A network can publish a local need or send a dynamic price signal, but someone still has to answer it with enrolled, dispatchable and verifiable capacity on that specific feeder. A marketplace can host offers, but the underlying fleet must be trusted, integrated and capable of reliable delivery. The network is building better ways to express local requirements. The customer-owned fleet still lacks a dependable way to respond.

This distinction matters. A signal is not the same as a service. An operating envelope is not the same as a trusted participation model. A tariff is not the same as a bankable, verifiable resource the DNSP can plan around. Without enough trusted flexibility underneath, even the best price signals and procurement platforms will under-deliver.

What “callable” should actually mean is therefore critical. It cannot mean the network or a third party simply takes control of a household battery. Most people did not buy storage to become a small utility asset. They bought it to reduce bills, use more of their own solar and retain control over their energy supply. Any model that ignores this reality will fail to attract participation at the scale required.

Callable must therefore mean available under clear, agreed rules while protecting the battery’s primary job: powering the home. Households should be able to set their own reserve levels, see when and why their battery was used, and opt out or adjust limits. They should be protected from opaque dispatch, uncompensated degradation and outcomes that leave them worse off. The battery should serve the household first, protect the household second, and only then offer surplus flexibility to the network.

The economic case for getting this right is straightforward. Customer-owned flexibility can often be cheaper than building more network capacity. Network augmentation enters the regulated asset base and is recovered from consumers over decades. If flexibility can safely defer or reduce that investment on some feeders, the savings are real and durable. To compete with copper, however, flexibility must become something a DNSP can understand and rely upon: a defined location, time window, quantity, performance standard, verification method and payment mechanism. Dynamic prices alone are not enough. Planners and financiers need something closer to a commitment.

The physical grid is becoming more local and dynamic. Rooftop solar reversed power flows. Batteries changed timing. Electrification and data centres are adding new load. At the same time, wholesale prices can fall while network charges continue to rise. A street can have abundant solar at noon and a transformer problem at dinner. The NEM was built for large generators, passive customers and regional prices. The distribution edge is now a world of active customers, flexible devices and local constraints. The early grammar of a more local system is appearing in projects like Edith, Flexible Exports and Piclo-style procurement. Grammar is not yet literature. The network is learning to express local needs more precisely. The harder task is building the trusted coordination layer that can turn millions of private devices into a dependable resource without removing control from the households that own them.

A fleet is not just a large number of machines. It is a collection of machines that can be coordinated for a purpose under agreed rules. A million privately owned batteries do not automatically become grid infrastructure. They become one only when there are clear interfaces, permissions, measurements, verification and payments that work across retailers and respect customer priorities. That is the stage Australia is now entering. The hardware is increasingly visible. The coordination layer is still forming.

The battery fleet is arriving. The network is learning how to ask. What remains is to build the trusted layer that can answer: a common phone number for local flexibility, without taking the battery away from the household that owns it.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

Australian Energy Market Commission. (2018). Coordination of generation and transmission investment: Final report. https://www.aemc.gov.au/sites/default/files/2018-12/CoGaTI%20Final%20Report.pdf

Australian Energy Market Commission. (2019). Coordination of generation and transmission investment: Directions paper. https://www.aemc.gov.au/sites/default/files/2019-06/CoGaTI%20Directions%20Paper.pdf

Australian Energy Regulator. (2025). State of the energy market 2025. Commonwealth of Australia. https://www.aer.gov.au/publications/state-energy-market-report/state-energy-market-2025

Australian Energy Regulator. (2025). State of the energy market 2025 – Chapter 2: National Electricity Market. Commonwealth of Australia. https://www.aer.gov.au/system/files/2025-08/State%20of%20the%20energy%20market%202025%20-%20Chapter%202%20-%20National%20Electricity%20Market.pdf

Australian Energy Regulator. (2025). State of the energy market 2025 – Chapter 3: Electricity networks. Commonwealth of Australia. https://www.aer.gov.au/system/files/2025-08/State%20of%20the%20energy%20market%202025%20-%20Chapter%203%20-%20Electricity%20networks.pdf

Australian Energy Regulator. (2025). State of the energy market 2025 – Chapter 6: Retail energy markets and energy consumers. Commonwealth of Australia. https://www.aer.gov.au/system/files/2025-08/State%20of%20the%20energy%20market%202025%20-%20Chapter%206%20-%20Retail%20energy%20markets%20and%20energy%20consumers.pdf

Ausgrid. (2025). Project Edith. https://www.ausgrid.com.au/Industry/Our-Research/Project-Edith

CitiPower, Powercor, & Piclo. (2025). Flexible markets partnership and procurement platform announcements. https://piclo.energy

SA Power Networks. (2025). Flexible exports. https://www.sapowernetworks.com.au/industry/flexible-exports/

Australian Competition and Consumer Commission. (2025). Inquiry into the National Electricity Market—December 2025 report. Commonwealth of Australia. https://www.accc.gov.au/about-us/publications/inquiry-into-the-national-electricity-market

Australian Energy Market Operator. (2025). Integrated system plan (ISP) 2025. https://aemo.com.au/energy-systems/major-publications/integrated-system-plan-isp

Discussion

Loading comments...