Why V2G needs to become boring

Issue 16: Where vehicle-to-grid is actually heading in Australia, and why

Vehicle-to-grid is no longer just about those giant EV batteries. Cheap home storage, collapsing midday power prices and smarter software are reshaping the economics. The future likely combines permanently connected home batteries with opportunistic EV flexibility, coordinated through increasingly automated energy markets.

Vehicle-to-grid (V2G) has been “almost here” for so long that many people have stopped noticing how much the surrounding economics have changed. The technology works. The demonstrations are compelling. Engineers love talking about it. Every few months another pilot program appears showing an electric vehicle powering a house, exporting into the grid or stabilising a local network. Yet it still has not happened at scale.

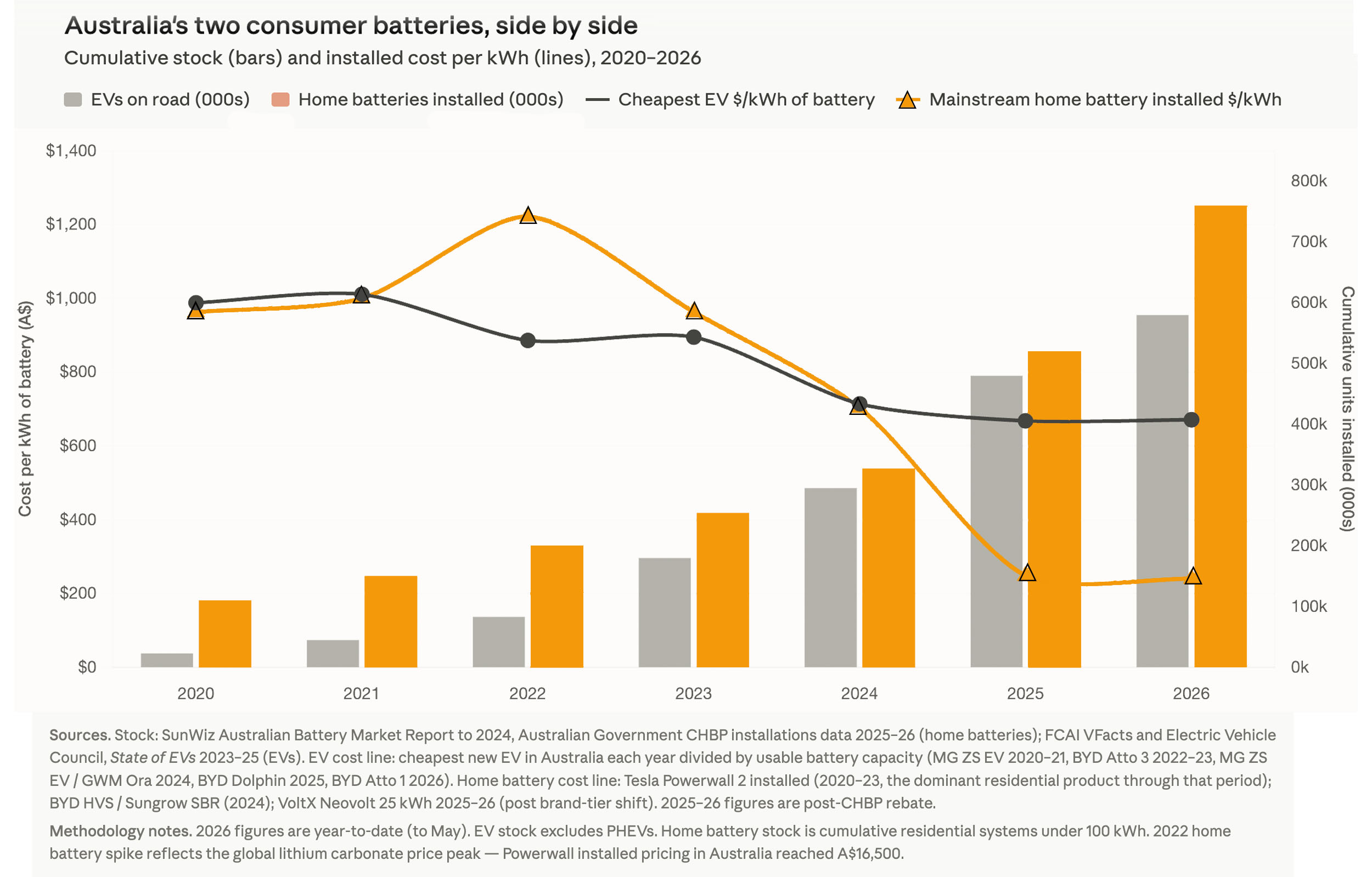

The original excitement around V2G was built on a simple idea. Electric vehicles contain enormous batteries. Most cars spend most of their time parked. Therefore the future electricity system would eventually consist of millions of giant mobile batteries connected to the grid whenever they were not being driven. Australia now has well over 500,000 EVs on the road, with adoption accelerating sharply through 2026, most carrying battery packs far larger than the average household storage system. In aggregate, the energy capacity is immense.

But the economics surrounding those batteries have changed dramatically.

The original V2G thesis rested heavily on the assumption that EV batteries would always be cheaper than standalone storage because car manufacturers were the only buyers purchasing lithium-ion cells at truly enormous scale. A few years ago, people were fond of saying things like “buy a battery in an EV and you get the car for free”. The logic was that a 75 kilowatt-hour (kWh) EV often cost little more (sometimes, even less) than a stationary battery of similar size.

That was broadly true for much of the early EV transition. The past few years have begun to tell a very different story.

Home battery costs collapsed just as deployment accelerated. The key shift is not simply that batteries became cheaper, but that permanently connected household batteries became substantially cheaper than mobile EV storage on a usable-per-kWh basis.

The Australian Federal Government’s Cheaper Home Batteries Program, introduced in July 2025, accelerated the shift by subsidising batteries for homes and small businesses. Although the subsidy was designed to cover around 30% of system costs, aggressive discounting by mainly Chinese suppliers often pushed effective reductions far higher. Home batteries rapidly became a mass-market product and the cost per kWh of stationary storage fell dramatically relative to batteries bundled inside EVs. They now cost less than half as much.

That changes the economics of V2G profoundly because EV batteries are no longer competing against expensive niche storage systems. They are competing against cheap, subsidised, permanently connected household infrastructure. We cover Australia's home battery phenomenon in Australia is winning the battery race. Now what?.

The comparison is revealing. Home batteries are much smaller than EV batteries, but they are always connected. They are already integrated into rooftop solar systems, already installed by the solar industry and sometimes even enrolled in virtual power plants. EV batteries are much larger, but they are mobile assets. They are not always home, not always plugged in and not always available during periods of peak demand.

The car battery is bigger. The home battery is there.

For most households, that matters more than sheer battery size because energy needs beyond roughly a day of household consumption often have sharply diminishing value. A permanently connected home battery may actually deliver more reliable grid value per kilowatt-hour than a much larger EV battery constrained by transport needs.

At the same time, the shape of Australia’s electricity market has changed dramatically. As discussed in The grid squeeze: Our grid is not full, but we keep building it and Free power at lunch and the democratisation of energy storage, rooftop solar has transformed the middle of the day into a period of abundance. Wholesale prices increasingly collapse toward zero and often below it during daylight hours. By early evening, when solar output disappears and demand returns, electricity becomes valuable again. The phenomenon is explained in our Battling Entropy primer What is the Duck Curve and why does it matter?.

The result is a system increasingly organised not simply around generation, but around timing. The value of storage increasingly comes not from storing enormous quantities of energy, but from moving comparatively small amounts of energy across increasingly volatile periods of time.

Aspire to be boring

That means the future of V2G is probably not a story about giant batteries alone. It is a story about coordination, connection and economics by many players in our National Electrity Market and a few outside it. A battery inside a car is not automatically part of the electricity system. It only becomes useful to the grid when an entire stack of technologies and institutions lines up around it: standards, chargers, electricity distributor (DNSP) approvals, retailer products, software coordination, customer behaviour and manufacturer warranties.

Until that stack becomes ordinary, V2G remains a demonstration rather than infrastructure. That is why the key threshold is not technical success. It is boredom. V2G becomes mainstream when it becomes boring.

Customers must be able to buy a compatible vehicle, install a charger through a repeatable process, connect it to a retailer product and largely forget about it. The system must quietly optimise charging and discharging in the background while preserving the thing the customer actually cares about: mobility. Rooftop solar crossed that threshold years ago. Home batteries are rapidly approaching it. V2G has not crossed it yet.

Australia today sits somewhere between proof-of-concept and early commercialisation. Nissan Leafs using CHAdeMO-based bidirectional chargers have participated in Australian trials for years, although hardly anybody uses CHAdeMO any more (or Nissan Leafs). Amber Electric has experimented with wholesale-linked charging and export. The ACT’s REVS project demonstrated that EVs could support homes and the wider grid. AGL launched a broader residential V2G trial in 2024 involving Hyundai, Kia, BYD and Zeekr vehicles.

The real question is no longer whether V2G works technically, but whether the commercial stack can work routinely. Can retailers manage the customer relationship? Will DNSPs approve exports? Will manufacturers stand behind warranties? Can installation become routine rather than bespoke?

The shape of that coordination challenge is increasingly pushing the market toward two distinct technical pathways.

AC / DC

In a DC bidirectional system, the wall charger performs most of the electrical work, converting power between the vehicle battery and the grid. This is how most early V2G systems operated, including the Nissan Leaf ecosystem. The approach works well technically, but it is expensive. Residential DC bidirectional chargers in Australia can easily cost between A$8,000 and A$15,000 installed once switchboards, electrical work and site complexity are included. Typical export capability sits around 12 kW, comfortably enough to support an average household.

AC bidirectional systems reverse the architecture. Much of the conversion happens inside the vehicle using the onboard inverter, making the wall equipment simpler and potentially far cheaper. Tesla’s recent AC-based bidirectional architecture in California matters because it points toward this possibility. Residential installations begin to look less like miniature industrial power stations and more like regular EV charger installations.

Export power in AC systems is somewhat lower, 7 kilowatts is common for many modern EVs. Yet that may not matter nearly as much as people think. Most Australian homes rarely require more power than that for sustained periods. An AC bidirectional system is already capable of running the home, shifting evening demand, supporting blackout backup and participating in virtual power plants.

If you have a modern EV it may already have a vehicle-to-load (V2L) feature allowing you to plug in individual appliances. What is involved in turning V2L into V2H and V2G? This mainly involves adding the systems that allow the car to synchronise safely with the household and wider grid. Tesla’s recent AC-based bidirectional architecture in California points toward this possibility.

This is why AC systems are likely to dominate the residential market. The history of electrification strongly suggests that the cheaper scalable architecture usually wins, even when technically more powerful alternatives exist.

DC systems still matter enormously in commercial settings because bypassing the vehicle’s onboard inverter allows much higher power, tighter control and infrastructure-scale aggregation. Their natural home is likely to be fleet depots, workplace charging hubs, logistics centres and commercial parking stations rather than suburban garages.

A parked fleet vehicle has something a household EV often does not: predictable availability.

Once vehicles stop behaving like household assets and start behaving like managed fleet infrastructure, the economics change completely. A commercial parking station filled with bidirectional EVs effectively becomes a distributed grid battery. Operators can aggregate power, arbitrage wholesale prices and provide network support services continuously rather than occasionally.

This is where the phrase “get paid to park” begins to make real sense.

Australia therefore probably does not end up choosing between home batteries and V2G. Instead, it develops layered forms of storage. Home batteries become the default stationary storage fleet quietly smoothing rooftop solar and evening demand. EVs become a second, more opportunistic layer providing additional flexibility, backup power and high-value support during periods of network stress or elevated wholesale prices.

The race to coordinate

The future may look less like “cars replacing home batteries” and more like an increasingly coordinated storage ecosystem in which rooftop solar generates energy, home batteries stabilise households, EVs provide surplus flexibility and software orchestrates the whole thing.

That coordination layer matters enormously. The real value of distributed batteries emerges not from individual devices but from fleets acting together. A single EV exporting into the grid is interesting. Hundreds of thousands responding to price signals and network conditions begin to look like infrastructure.

This is why, for V2G to go mainstream, all of these have to be aligned:

- Utility / network: the party that permits and values export into the grid

- Retailer or aggregator: the party that turns export into a customer product and revenue stream

- Vehicle manufacturer: the party that enables bidirectional operation and protects the battery warranty

- Equipment manufacturer / installer: the party that supplies certified chargers, gateways, inverters and switchgear

In some markets the Utility and retailer roles may be combined in a single integrated electrical utility. In Australia's NEM, there are separate network (DNSP) and retail/aggregator roles. This makes coordination more complex.

The vehicle manufacturer is an important part of any scalable V2G offering. Their standard battery warranties exclude battery cycling for external loads. Battery cycling limits have been a real economic drag on V2G. Although China is introducing solid-state EV batteries which will greatly reduce cycling degradation (explored in China's solid-state battery standard is about V2G, not range), EV manufacturers have dealt themselves a seat at the table on any V2G rollout through their warranty constraints.

No single player can solve V2G alone because V2G is not one technology. It is an ecosystem trying to coordinate itself.

Global action

Globally, different regions are converging toward this future through very different pathways.

In the United States, California remains the most visible residential testbed, with PG&E running Vehicle-to-Everything pilots that let customers use EV batteries for outage backup, arbitrage cheaper charging against expensive 4–9pm power, and earn incentives by exporting during high-demand events. The new development is that Tesla’s Cybertruck, Powershare Gateway and Universal Wall Connector have now been approved for PG&E’s residential V2X program, making California the first serious test of Tesla’s AC-based residential V2G architecture. This system only required two players, not four, because PG&E encompasses both the Australian DNSP and retailer roles while Tesla is both the vehicle manufacturer and connection equipment supplier. Texas has a different system. Tesla’s Powershare Grid Support is now available for many Cybertruck owners, provided they have Powershare equipment installed, enroll in the Tesla Electric Drive plan and opt in through the Tesla app. Tesla functions as roles 2, 3 and 4 simultaneously (retailer, vehicle manufacturer, equipment supplier), leaving only the distribution network — Oncor, CenterPoint or AEP Texas depending on the customer's location — as a separate party. Elsewhere in the US, the most concrete deployments are still fleet-led rather than household-led. Electric school buses now have V2G programs spread across 26 utilities and 19 states. The American pattern is becoming clear: California is testing residential architectures, Texas is testing Tesla-as-energy-retailer, and the most dependable near-term grid resource is still parked fleet vehicles with predictable schedules.

China is moving faster, but through a very different model. The National Development and Reform Commission has approved 30 large-scale V2G pilot projects across nine cities, including Beijing, Shanghai, Tianjin, Guangzhou, Shenzhen, Chongqing, Chengdu and Wuhan, with projects spanning private charging piles, heavy-truck charging and swapping stations, battery-swap stations, ports, factories, parks and city-level virtual power plants. This is not a suburban driveway story. It is infrastructure-led, city-led and grid-led. In China, all four key V2G roles are coordinated by the state (even BYD is state-adjacent). China plans thousands of bidirectional charging stations by 2027, but the commercial model is still young, with high equipment costs, state-controlled electricity pricing and battery-degradation concerns still holding back mass-market adoption.

Europe is making a slow start. Norway is proof that EV adoption is not always linked to V2G deployment. EVs were 96% of new passenger-car registrations in 2025, but V2G remains only at trial-stage. In Europe, the more important practical example is probably Utrecht in the Netherlands: the 'Utrecht Energised' project is roughly a year into a 500-vehicle rollout — 50 Renault 5 E-Techs went live in mid-2025 and have already dispatched 65 MWh and contributed up to 300 kW during evening peaks. Utrecht's four roles are filled by three parties: Stedin (grid operator), Renault (vehicle manufacturer with Mobilize's V2G toolkit), and We Drive Solar — which holds both the retailer/aggregator role and the equipment supplier role, simplifying coordination without going all the way to Tesla-style vertical integration.

Australia sits in a somewhat awkward intersection. It possesses something uniquely valuable: a deeply decentralised consumer energy culture. Australians already understand rooftop solar, home batteries, wholesale-linked tariffs and household energy arbitrage in ways most countries still do not. Australia’s EV fleet is increasingly Chinese in origin, reflecting BYD’s rapid rise alongside Tesla and other established players. China itself has not yet embraced the EV primarily as suburban electrical infrastructure, which creates an intriguing possibility: Australia may become one of the first countries to normalise the EV as part of everyday household energy systems.

However, we face particular challenges in securing the four partners needed to implement V2G. Our electricity retail market is fragmented and we have no obvious EV manufacturer to lead the way (as Tesla does in Texas by filling 3 of the 4 necessary roles). How do we know when we might have the participants needed for a serious rollout? I would be looking for a partnership involving a retailer/aggregator, a major DNSP and an EV manufacturer (BYD?) as a full partner with two-way battery cycling warranty support. If the rollout is AC-based for home use, the equipment will be less critical and several manufacturers may be able to fill that fourth slot. Australia's coordination challenge is harder than California's or China's. But the demand side conditions — rooftop solar saturation, household-level wholesale tariffs, mass-market batteries — give Australian consumers reasons to push through that coordination friction that consumers in other markets simply lack.

Storage is no longer becoming exceptional. It is becoming structural. The electricity system is evolving from one organised almost entirely around generation into one organised around generation, timing, coordination and flexibility. Some of those batteries will sit quietly on garage walls. Others will sit on driveways or inside fleet depots. The important point is that they are beginning to behave less like appliances and more like infrastructure.

New to this topic? See these Battling Entropy Primers to get you up to speed:

Get more like this

New analysis delivered to your inbox. No spam, unsubscribe anytime.

Take care, Tony

Disclosure: Battling Entropy is my independent commentary. The views expressed are my own and do not represent those of any organisation unless explicitly stated. This is not financial or investment advice.

I also have commercial interests in the energy technology field. I am working on a venture, Petajoule Capital, which is developing People-Powered Energy: one particular approach for the coordination of consumer-owned batteries, EVs and flexible demand. This article discusses issues relevant to that work.

Sources / Further Reading

ACT Government. (2023). The future of vehicle-to-grid (V2G) in Australia. https://www.cmtedd.act.gov.au/open_government/inform/act_government_media_releases/rattenbury/2023/the-future-of-vehicle-to-grid-v2g-in-australia

AGL. (2025, September 24). AGL puts wheels in motion with innovative vehicle-to-grid trial. https://www.agl.com.au/about-agl/news-centre/2025/september/agl-puts-wheels-in-motion-with-innovative-vehicle-to-grid-trial

Amber Electric. (2025, August 1). Lessons learned on V2G: Trial updates, early results, and next steps. https://www.amber.com.au/blog/lessons-learned-on-v2g-trial-updates-early-results-and-next-steps

Australian Energy Market Commission. (n.d.). National Electricity Rules. https://www.aemc.gov.au/regulation/energy-rules/national-electricity-rules

Australian Energy Market Operator. (2024). 2024 Integrated System Plan. https://aemo.com.au/energy-systems/major-publications/integrated-system-plan-isp/2024-integrated-system-plan-isp

Australian Government Department of Climate Change, Energy, the Environment and Water. (2026). Cheaper Home Batteries Program. https://www.dcceew.gov.au/energy/programs/cheaper-home-batteries

Australian Renewable Energy Agency. (2024). Amber: Automating EV charging in line with wholesale pricing. https://arena.gov.au/projects/amber-automating-ev-charging-in-line-with-wholesale-pricing/

Australian Renewable Energy Agency. (2026). Realising Electric Vehicle-to-Grid Services. https://arena.gov.au/projects/realising-electric-vehicle-to-grid-services/

Clean Energy Council. (2024). 4777.2 inverter standards change and product listings. https://cleanenergycouncil.org.au/industry-programs/products-program/inverters/standards-change

Clean Energy Council. (2025, March 17). Rooftop solar and storage report: July–December 2024. https://cleanenergycouncil.org.au/news-resources/rooftop-solar-and-storage-report-july-to-december-2024

Ferguson, A. J. (2026). The Cheaper Home Batteries Program. Battling Entropy Primer. https://battlingentropy.com/

Ferguson, A. J. (2026). The grid squeeze: Our grid is not full, but we keep building it. Battling Entropy. https://battlingentropy.com/

Ferguson, A. J. (2026). Free power at lunch and the democratisation of energy storage. Battling Entropy. https://battlingentropy.com/

Ferguson, A. J. (2026). What is the Duck Curve and why does it matter? Battling Entropy Primer. https://battlingentropy.com/

Institute for Energy Economics and Financial Analysis. (2024). Integrated System Plan needs greater ambition on DER to be a true whole-system plan. https://ieefa.org/resources/integrated-system-plan-needs-greater-ambition-der-be-true-whole-system-plan

PG&E Corporation. (2026, April 20). PG&E and Tesla turn Cybertruck into a grid asset, advancing the future of electric power in California. https://investor.pgecorp.com/news-events/press-releases/press-release-details/2026/PGE-and-Tesla-Turn-Cybertruck-into-a-Grid-Asset-Advancing-the-Future-of-Electric-Power-in-California/default.aspx

Renault Group, MyWheels, We Drive Solar, & Municipality of Utrecht. (2025, June 5). Utrecht becomes Europe’s first city with a vehicle-to-grid (V2G) car-sharing service. Renault Group Media Centre. https://media.renaultgroup.com/utrecht-becomes-europes-first-city-with-a-vehicletogrid-v2g-carsharing-service/?lang=eng

Standards Australia. (2024). What’s new in AS/NZS 4777.1:2024? Key updates for inverter energy systems. https://www.standards.org.au/blog/as-nzs-4777-updates

Tesla. (n.d.). Powershare. https://www.tesla.com/powershare

Discussion

Loading comments...